What The Bank Credit Card Risk Actually Is

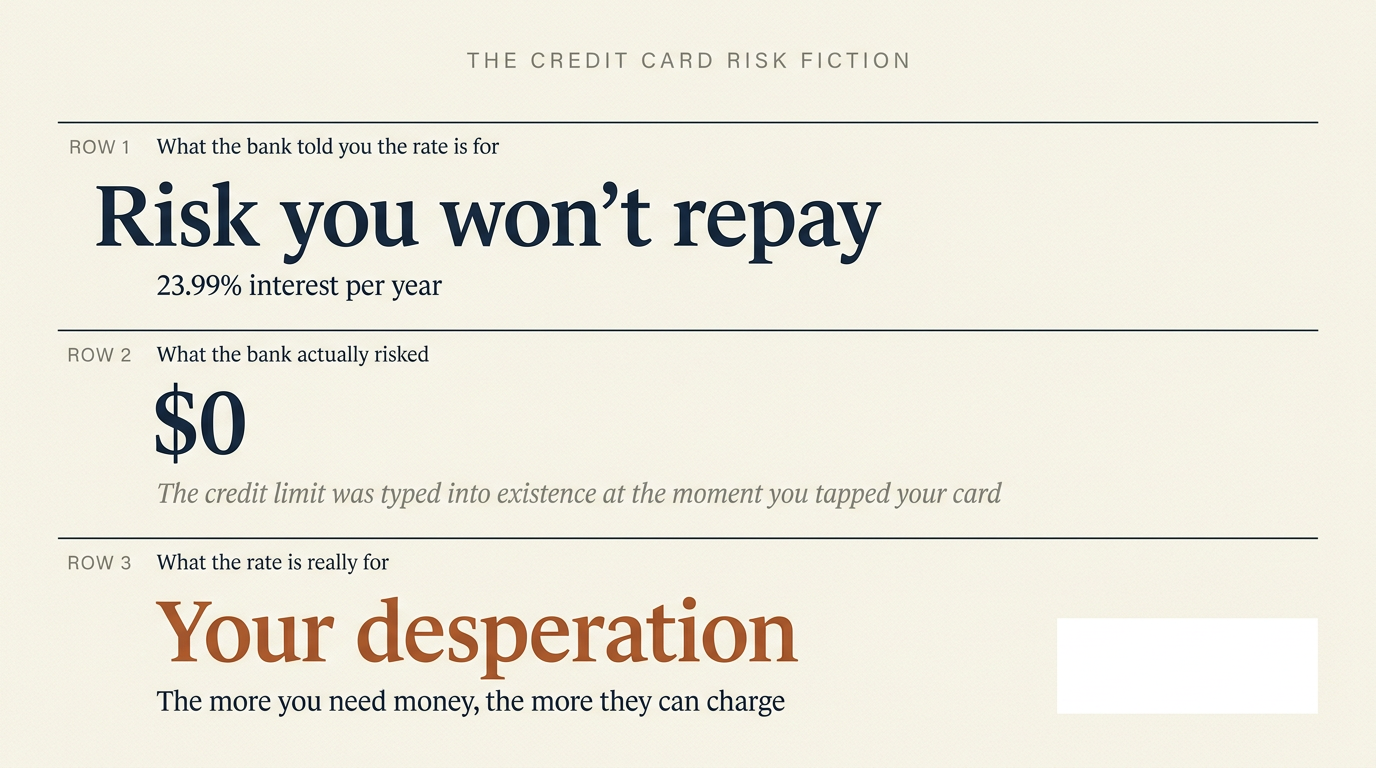

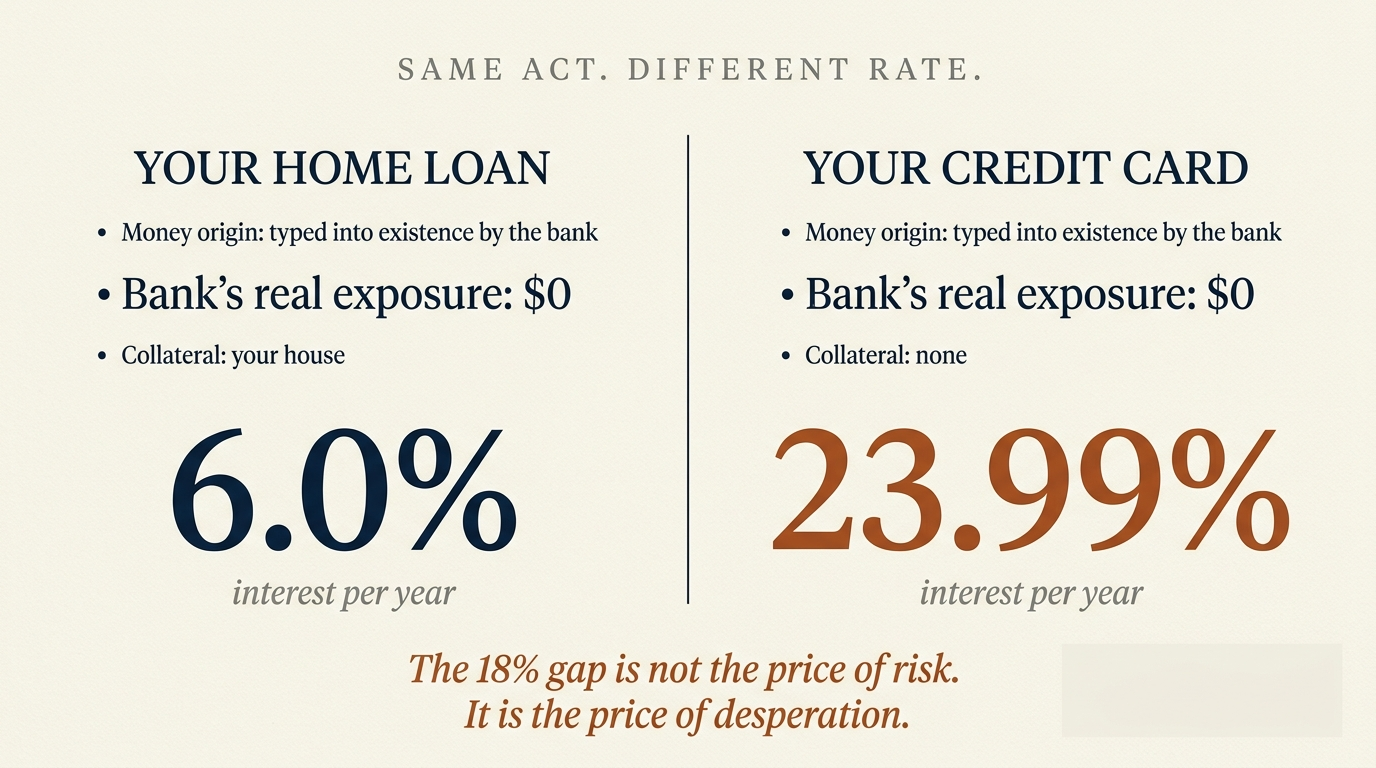

Have a look at this. You have a home loan at around 6%. You have a credit card at around 24%. Both loans came from the same bank. Both loans were created the same way. The bank wants you to believe the rate gap is the price of risk. It is not. The rate gap is the price of your desperation.

If you’ve read Money From Nothing and The Cup Of Water, you already know the mechanism — banks create money when they lend. The credit card piece slots on top of that. It is the same machine, with a different price tag, sold to a different customer in a different mood.

What The Bank Tells You

When you opened your credit card, the rate disclosure said something like 19.99% or 23.99%. If you have ever asked anyone at the bank why the rate is so much higher than a mortgage rate, you got some version of this answer:

“Credit cards are unsecured. There is no house to repossess if you don’t pay us back. That makes them high-risk lending. The high interest rate is what compensates us for that risk.”

— What the bank told you. Standard industry answer.

It sounds reasonable. It is the standard answer. It is what is taught in business school. It is what financial regulators officially accept as the justification for the rate.

It is also, when you look at it for one minute, not true.

What Actually Happened When You Tapped Your Card

When the bank issued your credit card with a $20,000 limit, no money was set aside. No vault was filled. No saver’s deposit was reserved. The $20,000 was a pre-authorisation to create up to that amount of new money the moment you started spending.

The first time you tapped the card at a coffee shop for $5, here is exactly what happened:

- The bank typed $5 of new money into existence at the moment of the tap.

- The bank credited the merchant’s account with $5.

- The bank added $5 to your credit card balance — money you now owe back.

The bank gave up nothing. Not a saver’s deposit. Not their own reserves. Not anything that existed before the tap.

By the time your statement arrives and you owe a $5,000 balance, all $5,000 was created by the bank at the moments you swiped. Not transferred. Not lent from existing funds. Created.

This is the same act described by the Bank of England in 2014, the act the entire NoticedYet thesis hangs on. A credit card is just a mortgage in fast-food packaging. Same machine. Different paperwork.

So What Did The Bank Actually Risk?

Trace it. They created the money from nothing. They never possessed it before the loan. They never gave up the use of any real asset to make the loan.

If you repay them in full, they receive the money back. Your repayment is destroyed on their balance sheet (the asset “loan receivable” goes to zero, the liability “your account balance” goes to zero, both sides shrink). They keep the interest you paid. The interest is real money you earned, transferred to them, in exchange for the privilege of using money they conjured.

If you do not repay them — if you default — what did they lose?

This is the critical question.

The bank’s balance sheet records a loss. The “loan receivable” of $5,000 disappears without a matching repayment. On paper, the bank is $5,000 worse off than the moment before you defaulted.

But the bank never gave up $5,000 of any real thing. They typed $5,000 into existence and you spent it. The real loss, in terms of actual economic resources, was borne not by the bank but by the economy — by every other holder of money whose purchasing power was slightly diluted when you spent the conjured $5,000 into the market.

In economic substance, the bank’s loss on a default is the loss of future interest income — the stream of payments they expected from you. They are not losing the principal because they never had the principal.

The Quiet Math Of Credit Card Default

A $5,000 default costs the bank a few hundred dollars in foregone interest, not $5,000 of principal.

The principal was never theirs. They typed it into existence. The “loss” they record is an accounting unwind of money that did not exist before they made the loan.

So is the bank’s real risk on credit card lending high? No. It is meaningfully lower than they ever say out loud.

Then Why Is The Rate 24%?

The answer is simple and it is the centre of this post.

The bank charges what the borrower will pay.

A homeowner shopping for a mortgage is generally not in distress. They have time. They have multiple lenders competing for their business. They can walk away. They might even be talking to a mortgage broker who shops the market. The market is competitive. The rate gets driven down to something around the cost of the bank’s own wholesale funding plus a healthy spread.

A person standing at a checkout with a maxed-out fortnight, three days from payday, a car registration due, and a credit card in their wallet is not in that position. They are not shopping. They are not comparing. They are reaching for the card because the alternative is “this transaction does not happen, and something breaks.”

The bank knows this. The rate the bank charges on the credit card is calibrated not to the bank’s risk but to the borrower’s lack of options.

The 6% home loan and the 24% credit card are not priced on different risks. They are priced on different desperations.

A Worked Example

Suppose Mrs. Smith of Liverpool wants to spend $5,000. She has two ways to borrow it from the same bank that holds her mortgage:

Money creation mechanism: identical. Bank’s real economic exposure: identical (both effectively $0). Bank’s profit if she repays: four times higher on Option B.

The 18% interest rate gap is not the price of risk. The bank’s exposure is essentially the same in both cases. The gap is the price of which mood Mrs. Smith was in when she chose the product.

In Option A, she was at the kitchen table on a Sunday, comparing lenders, with time to shop.

In Option B, she was at a checkout on a Friday afternoon, three days from payday, with no time to shop.

The bank takes the gap. The bank tells you it is for risk. It is for something else.

A Quiet Invitation

If this is changing how you read your credit card statement, the next post in your inbox is going to land hard.

When This Lands Hardest

The desperation premium is steepest on the people with the fewest options. Payday lenders charge effective annual rates of 400% or more for the same act — typing money into existence at the moment a borrower needs it. Those rates are not the price of risk either; they are the price of “the alternative is the gas getting cut off.”

Buy-now-pay-later schemes charge merchants 4-6% of every transaction and load late fees on consumers. Same act. Same conjured money. Same desperation pricing wrapped in friendlier-looking app branding.

Pawn shops, debt consolidators, hire-purchase furniture chains, vendor finance on used cars — all variations of the same theme. The poorer you are, the higher the rate, regardless of any actual risk to the lender.

This is why the credit card “high risk” framing matters. If we accept it, every other rate above it is also “risk-based” and therefore justified. If we reject it — and the moment you look at the mechanism, you have to — then the entire pricing hierarchy of consumer credit is revealed for what it is: a graduated tax on financial vulnerability.

Three Questions Everyone Should Ask

The desperation premium is built to make these three questions impossible to dodge.

Get The Next Post By Email

One plain-English post at a time. No tracking pixels. No advertising. Unsubscribe in one click. Your email goes to [email protected] and nowhere else.

Have you noticed yet?

Frequently Asked Questions

Don’t credit card defaults really hurt the bank?

The bank takes an accounting loss equal to the unpaid balance. But that balance was money the bank created from nothing — they never gave up the use of any real asset to make the loan. The real economic loss to the bank is mostly the foregone future interest, not the “principal.”

What about the bank’s funding costs?

Banks fund their lending primarily from deposits (which they pay near zero on) and the wholesale market (which they pay close to the cash rate on). Even adjusting for those, the cost-of-funds explains the home loan rate of 6% reasonably well. It does not explain a credit card rate of 24%.

Aren’t credit card borrowers riskier as a group?

Yes, in the sense that defaults are more common on unsecured revolving credit than on first-mortgage debt. But the rate differential the banks charge is far larger than the actual realised default rates justify. Big bank credit card portfolios are reliably profitable through every business cycle. The defaults do not eat the interest — they are a small fraction of it.

Is this true for buy-now-pay-later too?

Substantially yes. BNPL operates on the same money-creation principle — credit extended at point-of-sale, repayment expected later. The merchant fee plus late-fee model is the same desperation pricing in a different costume.

What about Islamic finance? Does it dodge any of this?

Some Islamic credit products explicitly forbid riba and structure as profit-sharing or asset-based. The structural critique here — the act of money creation while taking real labour in exchange — applies to any system that lets a lender originate purchasing power without giving up real value. Some Islamic finance avoids that; some technically conforms while replicating the substance.

What can I personally do about credit card debt?

Pay it down before any other goal. The 24% you pay is real labour disappearing into nothing in exchange. Refinance into the lowest-rate facility you can access (often the home loan, if you have one). This blog does not give financial advice; this is observation, not recommendation. Speak to a fee-only adviser before changing any product.

About The Author

M. Notice

M. Notice writes NoticedYet, a calm, sourced blog about how private commercial banks create money out of nothing and what that means for the rest of us. The pen name is a voice choice, not opsec. Every post is primary-source-anchored. No products endorsed. No politicians backed.

Reach out: [email protected]

Sources

- McLeay, Radia, Thomas. “Money creation in the modern economy.” Bank of England Quarterly Bulletin, Q1 2014.

- Reserve Bank of Australia. Statistical Tables — credit card and personal lending series.

- Australian Securities and Investments Commission. Credit and consumer credit regulatory resources.

- Australian Competition and Consumer Commission. Reports on competition in consumer banking.

- Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. Final Report (Hayne, 2019).

- Center for Responsible Lending — research on the structural economics of consumer credit pricing.

- Hyman Minsky. Stabilizing an Unstable Economy. Yale University Press, 1986.

Information about the banking system, credit products, and regulation changes over time. Linked content may move or be updated without notice. This article is general information and analysis only and is not financial advice. Always seek advice suited to your personal circumstances from a qualified, fee-only adviser whose interests are not tied to product sales. Please verify the primary sources for yourself — that is half the point.