Buying Your Hard-Built Business With Conjured Money

You spent twenty years building a small business. Light manufacturing, say. Or a regional accounting practice. Or a chain of three suburban cafes. You started in your garage. You found your first customers by knocking on doors. You hired your first staff. You built relationships. You built a brand. You built equity in something that did not exist before you did the work.

Then the squeeze comes. Inflation eats your margins. Interest rates rise. Your working capital line gets more expensive. Customers slow down their payments. The bank notices. The bank gets nervous.

Then the offer comes. A larger company — or, more often these days, a private equity vehicle — offers to buy you out. The number sounds large. You are tired. You are stretched. You sign.

The money you are paid was created by a bank the moment the buyer signed the loan to acquire you. It cost the bank nothing to make. It cost the buyer almost nothing to use. You handed over twenty years of real work and they handed over ledger entries.

This is one of the quieter and most destructive operations of the credit-creation system. If you have read Money From Nothing, The Cup Of Water, What The Bank’s Credit Card “Risk” Actually Is, and Why Your Grandfather Lived Off His Savings And You Cannot, you have the mechanism. This post is what the mechanism does to the real productive economy.

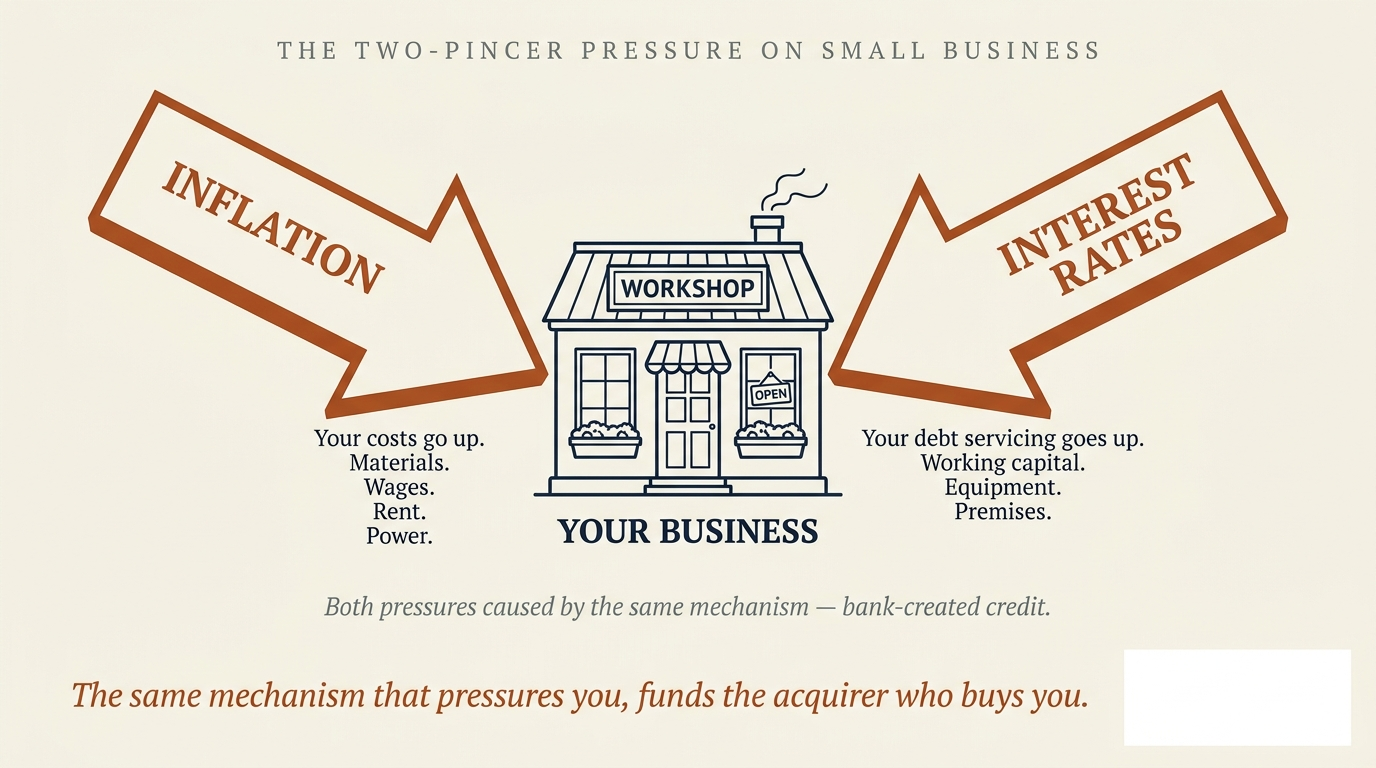

The Two-Pincer Pressure

A small business under pressure today is under pressure from two directions, and both directions trace back to the same place.

From above, inflation. Your input costs go up year on year. Materials cost more. Wages cost more. Power costs more. Rent costs more. The rate at which your costs rise is set by the broader money supply — itself driven, as we’ve covered, by bank credit creation. The more credit the banking system writes into the economy, the more dollars chase the same goods, the faster your supplier puts the price up.

From below, interest rates. To control the inflation it is itself fuelling, the central bank raises the cash rate. Your business loan, your overdraft, your equipment finance — all become more expensive. Working capital that used to cost you 4% now costs 9%. The same loan amount, the same business, the same balance sheet — but the debt servicing has more than doubled.

Both pressures are caused by the same engine: a banking system that creates money through lending. The first effect is inflation. The second effect, when the system tries to control the first, is a rate rise. Your business is the meat in the sandwich.

By the time both pincers have squeezed for a couple of years, you are tired. Margins have evaporated. The relationship with the bank has changed — from friendly business partner to nervous creditor. You are not bankrupt. But you are no longer prospering. You are surviving.

This is the moment the offer arrives.

The Offer

An email. A LinkedIn message. A phone call from a corporate adviser. Sometimes it’s a direct competitor who has weathered the squeeze better. Sometimes it’s a roll-up consolidator with a portfolio of similar businesses. More often these days, it’s a private equity vehicle with a deck full of synergies and a relationship with three commercial banks.

The offer is presented as relief. “We see the pressure you’re under. We’ve been watching the sector. We think there’s value here. We’d like to offer you a clean exit.”

The number is, on paper, large. Several times your annual profit. Sometimes ten times your annual profit. To a small business owner who has been treading water, this is life-changing money. It is the difference between retiring at 58 and retiring at 73.

You ask, naturally, “Where is the money coming from?”

The buyer answers, equally naturally, “Bank funding. Standard acquisition finance. We’re well-capitalised.”

You accept the answer because it sounds professional. What you are not told, because most sellers don’t ask, is what “bank funding” means in practice. You think the bank has the money sitting somewhere, and is lending it to the acquirer. The bank does not. The bank will type the money into existence at the moment the loan is signed. The acquirer will use that conjured money to buy you. The acquired business itself will be loaded with the loan, and the cash flows from the business will be used to service the debt.

This is called a leveraged buyout. It is the most common way medium-sized businesses change hands now.

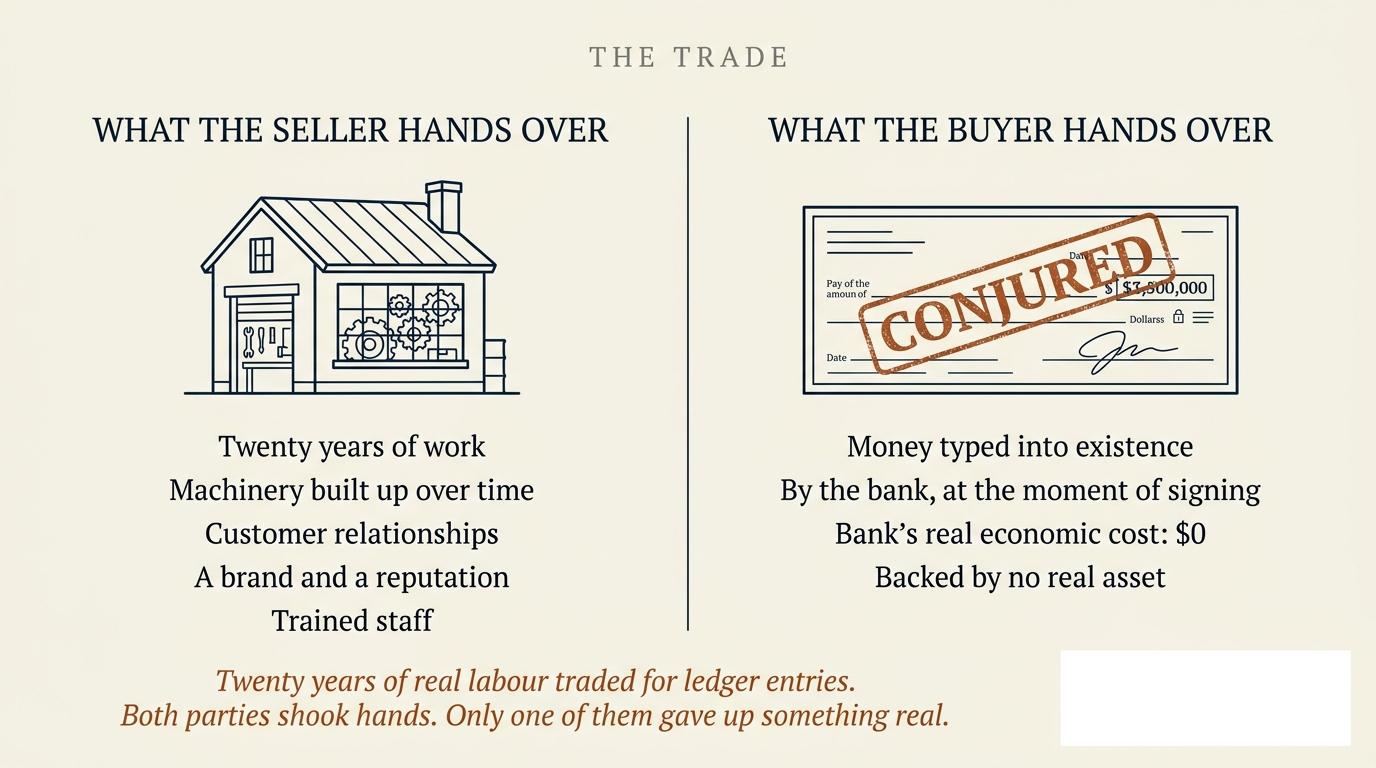

The Trade

What you actually traded:

- Twenty years of your working life.

- Equipment you bought one machine at a time, often by deferring your own pay.

- A customer base you cultivated by showing up when you said you would.

- A brand that meant something in your local market.

- Trained staff who knew how to do the work.

What you received:

- A sum of money the bank typed into existence at the moment the buyer signed the acquisition loan.

The money you received is, of course, real to you. You can spend it. You can buy a house with it. You can retire on it. The fact that the bank conjured it from nothing does not change the fact that it operates as money in the world.

But the deeper economic act of the transaction is this: twenty years of real productive output was transferred to a buyer who paid with ledger entries that cost the lending bank nothing to produce. The substance of your business has moved into other hands. The substance of what you received from them was conjured at the moment of the handshake.

You walked away. You spent the money. Some of it on a house. Some of it on superannuation. Some of it on the holiday you owed yourself. By the time you’ve made all the purchases, you’ve returned the conjured money to the economy — where it now sits, adding to the supply of money that other people are using to chase the same finite supply of goods.

The bank, which created the money in the first place, collects interest on the loan it wrote to the buyer. The buyer services that interest out of the operating cash flow of your acquired business. Over the next ten years, the buyer extracts considerable value from the business. They may strip non-core assets (the property you owned and operated from, for example). They may close marginal locations. They may consolidate operations into existing entities. They may load the acquired business with additional debt to pay themselves dividends. They may, eventually, sell it again at a multiple.

None of this returns the productive intent of your original work. It mostly extracts what you built.

The Quiet Math Of The Acquisition

A leveraged buyout takes a productive business, loads it with new debt the business itself must service, and transfers ownership using bank-created money.

Nothing real was paid for what was acquired. The seller walks away with cash. The bank collects interest. The business carries the debt. The community loses the family-owned, locally-rooted version of the operation.

The Cruel Symmetry

This is what makes the operation more than just “unfortunate market dynamics.”

The bank-credit-creation system caused the inflation that pressured your business. The same system caused the rate rises that strangled your working capital. Then the same system funded the acquisition by the larger buyer who took advantage of your weakened state.

The credit system was, simultaneously: (a) the pressure on you, (b) the relief from the pressure (in the form of “exit liquidity”), and (c) the engine that funded your replacement — the entity that now owns what you built.

Both ends of the transaction were funded by the same machine. The machine took a fee at both ends — interest on the working capital line that squeezed you, then interest on the acquisition loan that bought you out. Everyone whose hands the operation passed through paid the bank.

This is not a conspiracy. There is no smoke-filled room in which a banker decides to pressure your business so that a different banker can fund its acquisition. It is structural. The machine is built to do this. The machine does it efficiently, day in, day out, in every developed economy in the world.

The same mechanism that pressures you, funds the acquirer who buys you. The bank takes a fee at both ends.

— The structural sentence of the post.

A Quiet Invitation

If this is the first time you’ve seen the small-business buyout described this way, the next post should be in your inbox.

What This Means For The Economy You Live In

Over thirty years, this process has been running at an industrial scale across the Western economies. Family-owned manufacturers, regional accounting firms, small medical practices, hospitality groups, hardware stores, dental clinics, plumbing businesses, veterinary practices, mechanics, funeral homes, restaurants, beauty businesses — all of these have been absorbed by larger entities using bank-conjured acquisition finance.

The result is a less local, less diverse, less responsive productive economy. The decisions are made elsewhere. The profits flow elsewhere. The staff are managed by people who have never met them. The customer service degrades. The brand becomes plastic.

You feel this when you cannot get a tradie to come out. When your accountant retires and the firm is now part of a national chain with a 12-month wait. When the local hardware shop closes and the nearest replacement is half an hour away with a different range. When the family restaurant becomes a franchise. When the local newspaper is owned by a private equity vehicle three layers up.

None of this happened because consumers wanted it. It happened because the banking system was structurally biased toward funding the larger entity’s acquisition of the smaller. Bank-created money was always cheaper for the buyer than it was for the seller’s own working capital.

This is the consolidation tax on local productive economies. It is paid by everyone who lives in a town and uses what’s left of its businesses. It is paid mostly by the next generation, which inherits a less owned, less rooted, less responsive economy than the one their parents built.

Three Questions Everyone Should Ask

The leveraged-buyout machine is built to make these three questions impossible to dodge.

Get The Next Post By Email

One plain-English post at a time. No tracking pixels. No advertising. Unsubscribe in one click. Your email goes to [email protected] and nowhere else.

Have you noticed yet?

Frequently Asked Questions

Aren’t business sales a normal part of capitalism?

Sales of productive enterprises are normal. The structural feature this post critiques is that the buyer’s purchasing power is bank-created credit rather than real savings. Under a sovereign-money system, businesses would still change hands, but the buyer would have to use real saved capital. The price discovery would be honest. The pressure that softens up the seller would not exist.

Doesn’t private equity sometimes improve businesses?

Sometimes — particularly in distressed turnaround situations. The structural critique is not about every PE deal. It is about the funding mechanism that allows PE vehicles to outbid family successors, employee buyout groups, and other less-extractive acquirers. The credit-creation system tilts the playing field toward the most leveraged player.

What if I’m the seller and the money will fund my retirement?

This post is not advice and does not suggest you should refuse a fair offer. The cash you receive is real to you. The observation is about what the system extracts from local productive economies in aggregate. Many sellers have no choice; the squeeze leaves them no alternative. The critique is of the system, not the seller.

Can employee ownership work as an alternative?

Yes, in principle. Employee Stock Ownership Plans (ESOPs in the US) and similar vehicles allow staff to acquire the business gradually. They are structurally disadvantaged because they cannot match the leverage and speed of a PE bid. A sovereign-money system that did not provide cheap acquisition leverage to PE vehicles would level that playing field considerably.

Isn’t this just market efficiency — resources flowing to better operators?

“Better operators” presumes the buyers are deploying real saved capital in pursuit of long-term productive returns. When the capital is bank-conjured and the holding period is five to seven years before the next sale, the operator is not optimising for productivity. They are optimising for asset stripping and resale. That is not market efficiency. It is rent extraction wearing a market costume.

What would sovereign money change for small business?

Under a sovereign-money system, banks would lend real savers’ deposits. Working-capital lines for productive businesses would still exist, priced to compete for those savers. Acquisition leverage would be much more expensive. The two pincers described in this post would weaken substantially. Family ownership transitions and employee buyouts would become more competitive against PE bids. Local economies would consolidate less.

About The Author

M. Notice

M. Notice writes NoticedYet, a calm, sourced blog about how private commercial banks create money out of nothing and what that means for the rest of us. The pen name is a voice choice, not opsec. Every post is primary-source-anchored. No products endorsed. No politicians backed.

Reach out: [email protected]

Sources

- McLeay, Radia, Thomas. “Money creation in the modern economy.” Bank of England Quarterly Bulletin, Q1 2014.

- Bank for International Settlements. Working Paper 821 on private equity and leveraged buyout activity.

- Benes, Kumhof. “The Chicago Plan Revisited.” IMF Working Paper WP/12/202, August 2012.

- Australian Competition and Consumer Commission. Mergers and acquisitions reports.

- Eileen Appelbaum & Rosemary Batt. Private Equity at Work. Russell Sage Foundation, 2014 — foundational research on PE acquisition impacts.

- Joseph Huber. Sovereign Money: Beyond Reserve Banking. Palgrave Macmillan, 2017.

- Hyman Minsky. Stabilizing an Unstable Economy. Yale University Press, 1986.

Information about the banking system, leveraged buyouts, and corporate acquisition practices changes over time. The narrative example is illustrative. Linked content may move or be updated without notice. This article is general information and analysis only and is not financial, legal, or business advice. Always seek advice suited to your personal circumstances from a qualified, fee-only adviser whose interests are not tied to product sales. Please verify the primary sources for yourself — that is half the point.