If You Do Not Repay, Who Actually Loses?

When a borrower defaults on a loan, the bank cries loss. The accountants book the loss. The shareholders are told about the loss. The regulator monitors the loss. The bank uses the prospect of losses like this to justify the high interest rates they charge in the first place.

What, exactly, did the bank lose?

This is the question that makes the entire risk-pricing logic of consumer credit collapse on inspection. It is the question this post answers. It builds on Money From Nothing, The Cup Of Water, What The Bank’s Credit Card “Risk” Actually Is, Why Your Grandfather Lived Off His Savings And You Cannot, and Buying Your Hard-Built Business With Conjured Money. If you’ve read those, this one might rewire the way you read every news story about bank losses for the rest of your life.

The Bank’s Story About Default

The standard story goes like this:

- A bank lends a borrower $5,000.

- The borrower fails to repay.

- The bank loses $5,000.

- To compensate for the chance of this happening, the bank charges all borrowers an interest rate that includes a “risk premium” reflecting the average probability of default across the portfolio.

- This is why interest rates are positive, why they vary by borrower quality, and why credit cards cost more than mortgages.

Almost every official explanation of bank lending uses this story. Business school courses teach it. The Royal Commission accepted it. Treasury frames lending profitability through it. The big four banks’ annual reports recite it.

It is not true. Or rather, it is true at the accounting layer and false at the economic layer, and the difference between those two layers is the entire post.

What Actually Happens On The Bank’s Books

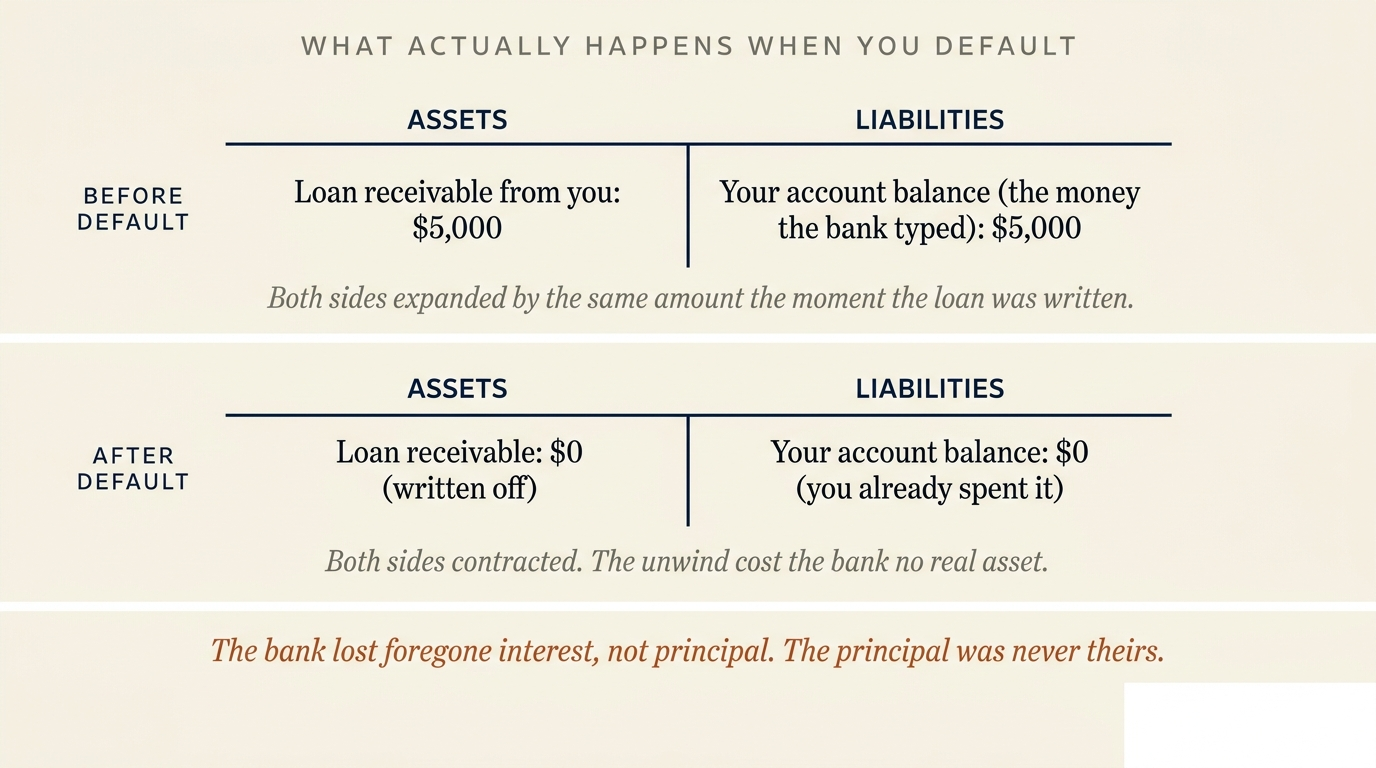

When the bank lent you $5,000, the balance sheet expanded by exactly that amount on both sides:

- Asset: “Loan receivable from you: $5,000”. This is the bank’s claim on your future repayment.

- Liability: “Your account balance: $5,000”. This is the deposit the bank typed into existence for you to spend.

This is the mechanism the Bank of England confirmed in 2014. The loan creates the deposit. Both sides of the balance sheet grow by the loan amount the moment the loan is written.

Now suppose you default. You stop paying. The bank, after some time, decides to write the loan off.

On the bank’s books:

- The “Loan receivable” goes to zero (the asset is written off).

- The “Your account balance” was already depleted (you spent the money long ago).

- Both sides of the bank’s balance sheet contract by the loan amount.

The accounting equation rebalances. The bank’s reported assets and liabilities both shrink. The bank’s equity — the difference between them — is unaffected by the principal of the writedown, mathematically speaking.

So what is the loss the bank’s annual report describes?

The Real Economic Loss To The Bank

The bank’s loss is not the principal. The bank’s loss is the future interest payments it expected to receive from you.

If you had repaid the $5,000 over five years at 24% interest, the bank would have received roughly $3,300 in interest payments over that time. Default at month three of the loan means the bank receives only about $150 of interest before the loan goes bad. The economic loss is therefore around $3,150 of expected future interest, not $5,000 of principal.

That’s still a meaningful loss. Banks lose real money on defaults — just not in the way the headline figure suggests. It’s about a third of what the official “loss” number says.

Add in the cost of collections, the operating expense of writing off the asset, regulatory capital charges, and reputational damage, and the bank’s real economic loss on a default is perhaps 40-50% of the headline number. Still nothing close to “they lost $5,000.”

The Quiet Reframe

When a borrower defaults, the bank’s real loss is the foregone interest, not the principal. The principal was never theirs to lose.

The risk premium baked into every interest rate is calibrated against a fictional loss number. Strip out the principal and the rate has no business being where it is.

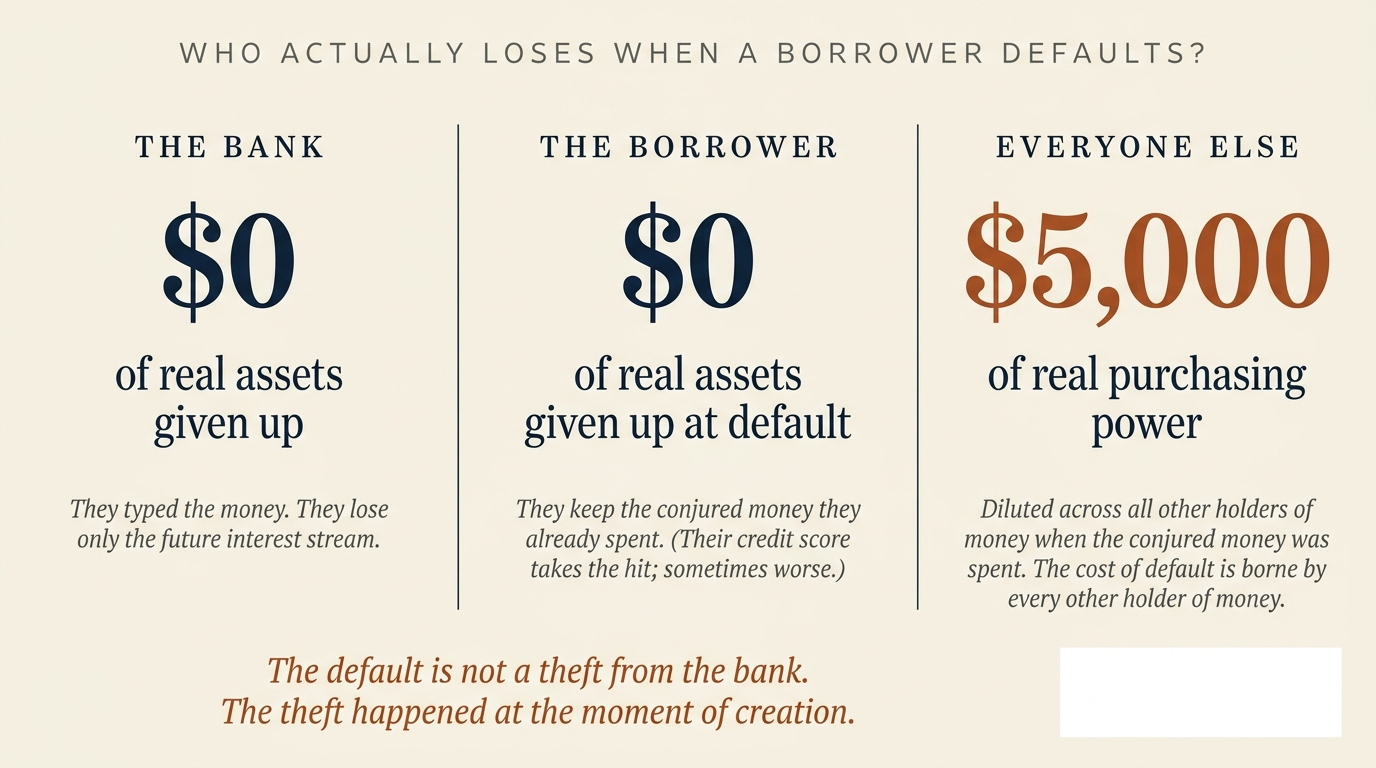

Who Actually Lost The Real Money?

This is the question very few people ask. The answer is uncomfortable.

The $5,000 that was “lost” went somewhere. Money doesn’t disappear without a trace, even when an accountant writes it off. So where did it go?

Trace it back. The bank created $5,000 the moment they wrote the loan. You spent the $5,000 into the economy — on a fridge, a holiday, an emergency dental bill, a course, whatever. The fridge seller received the $5,000. They banked it. From there it circulated, paying for other things, becoming part of the broad money supply.

When you default, the bank writes the loan off. But the money you spent is still circulating in the economy. The fridge seller still has their money. The fridge is still in your kitchen. The transaction at the merchant did not unwind.

What changed is the bank’s claim against you. The contract that said “you will return $5,000 to the bank, and the bank will destroy that money on receipt” no longer applies. The $5,000 of new money that entered circulation when the loan was written stays in circulation permanently — rather than being destroyed when you repaid.

So the economy now has $5,000 more money in it than it would have had if you had repaid. Every other holder of money — every wage-earner, every pensioner, every saver — has had their purchasing power slightly diluted by the new money you spent and never withdrew.

The real economic loss of your default is paid by everyone else holding the currency. The bank lost foregone interest. You kept the conjured money. The economy at large lost real purchasing power.

This is structurally identical to the inflation mechanism in The Cup Of Water. The same act — new money entering the market without new goods backing it — just made permanent because you didn’t repay. The desert worker’s $10 still buys half a cup, only this time forever.

The Bank’s Risk Premium Is Built On A Fiction

If the bank’s real loss on a $5,000 default is closer to $2,500 (the foregone interest plus collection costs), then the risk premium that justifies the high credit card rate is calibrated against the wrong number.

If you accept the standard logic that the rate compensates the bank for “average loss times probability of loss,” then halving the loss should halve the risk premium. The portion of the 24% credit card rate attributable to default risk should be much smaller than the public is told.

Take a typical Big Four credit card portfolio. Default rates are usually around 1-2% of balances per year. If a default costs the bank an average of $2,500 on a $5,000 balance (~50% of nominal), then the loss provision needs to be roughly 0.5-1% of the portfolio per year — not 5-10% as the bank’s risk premium math would imply if you took the “lost $5,000” story literally.

Put differently: if banks were calibrating risk premiums against their real economic losses, credit card rates would be much closer to home loan rates. They are not because the risk story is a justification, not a calibration.

The default is not a theft from the bank. The theft happened at the moment of creation. The default just means the conjured money is not destroyed at the end of the cycle.

— The structural sentence of the post.

A Quiet Invitation

If this is changing how you read every “bad debt provision” line in a bank’s annual report, the next post should land in your inbox.

What This Means For The Default Conversation

Two things change when you accept the reframe.

First, the moral weight of a borrower’s default shifts. The borrower has not stolen $5,000 from the bank. The borrower has kept money that the bank conjured into existence and that, on full repayment, would have been destroyed at the end of the cycle. The borrower’s default makes that money permanent in circulation, diluting every other money-holder’s purchasing power by an infinitesimal amount.

This does not make default victimless or virtuous. The borrower is still breaking a contract. The bank still incurs operating cost and lost income. Other holders of money still take a tiny dilution. But the “borrower stole from the bank” framing — which underwrites the entire collections industry, including aggressive debt-collection practices, wage garnishment, and bankruptcy proceedings — is built on an economic claim that does not stand up.

Second, the moral weight of bank profits shifts. When a bank reports record profits “despite high loan loss provisions,” the implicit claim is that the bank generated those profits in the teeth of real economic losses. The reality is that the bank’s reported loan losses are largely accounting unwinds of money they conjured in the first place. The “despite losses” framing flatters the bank. Strip the rhetoric and most reported bank profits are uncovered seigniorage — the gain from creating money, less the small real cost of operating the bank.

Three Questions Everyone Should Ask

The default reframe makes these three questions impossible to dodge.

Get The Next Post By Email

One plain-English post at a time. No tracking pixels. No advertising. Unsubscribe in one click. Your email goes to [email protected] and nowhere else.

Have you noticed yet?

Frequently Asked Questions

Are you saying banks don’t lose anything on defaults at all?

No. Banks lose real money on defaults — just not in the way the headline figure suggests. The real loss is roughly the foregone interest stream, plus operating cost of collections and writeoff, plus regulatory capital charges. That comes to perhaps 40-50% of the nominal “loss” figure on a typical retail default. Not zero, but very different from the public framing.

If banks don’t really lose principal, why do they pursue defaulters so aggressively?

Several reasons. First, the recovery improves their reported profitability. Second, aggressive enforcement deters future defaults across the wider portfolio, which is genuinely worth money to them. Third, the collections industry itself is profitable and creates downstream commercial value (sale of debt to collectors). Fourth, the legal and regulatory framework treats principal as a real asset, which is true at the accounting layer even though it is fictional at the economic layer.

Doesn’t the bank need to hold capital against potential losses?

Yes. APRA requires banks to hold regulatory capital against credit risk. That capital does represent real bank equity at risk. But the capital requirements are calibrated against accounting loss measures, not economic loss measures. If they were calibrated against economic loss, they would be much lower — which is exactly why the lobbying battles over capital requirements are so persistent.

What about depositors — aren’t they really the ones funding the loan?

No. Deposits are a byproduct of lending, not the source of it. The Bank of England’s 2014 paper is explicit on this. A bank can write a loan and the corresponding deposit appears in the borrower’s account simultaneously. The bank does not need to source deposits first to write the loan. Deposits become a funding consideration after the loan is on the books (for liquidity ratios), but they are not the raw material being lent.

If everyone else pays for defaults through inflation, isn’t that an argument against defaulting?

Yes — but it’s also an argument against banks creating credit in the first place. The dilution to other holders of money happens at the moment the loan is created, regardless of whether the loan is later repaid or defaulted. Repayment destroys the conjured money and partly undoes the dilution. Default leaves the money in circulation permanently. Neither is good. The structural problem is the act of creation, not the act of default.

Would sovereign money change how defaults work?

Yes. Under a sovereign money system, banks would lend real saved deposits. A default would mean a real loss to a real saver — the saver who funded the loan would not be repaid. That is a meaningfully different moral and economic situation. The borrower is genuinely taking money the saver gave up. The risk premium then becomes a real risk premium against real saved capital. The whole conversation about consumer credit becomes more honest.

About The Author

M. Notice

M. Notice writes NoticedYet, a calm, sourced blog about how private commercial banks create money out of nothing and what that means for the rest of us. The pen name is a voice choice, not opsec. Every post is primary-source-anchored. No products endorsed. No politicians backed.

Reach out: [email protected]

Sources

- McLeay, Radia, Thomas. “Money creation in the modern economy.” Bank of England Quarterly Bulletin, Q1 2014.

- Australian Prudential Regulation Authority. Credit risk capital requirements (APS 112, APS 113).

- Basel Committee on Banking Supervision. Basel III credit risk framework.

- Reserve Bank of Australia. Banking sector statistical tables — provisions and impaired assets.

- Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. Final Report (Hayne, 2019).

- Joseph Huber. Sovereign Money: Beyond Reserve Banking. Palgrave Macmillan, 2017.

- Benes, Kumhof. “The Chicago Plan Revisited.” IMF Working Paper WP/12/202, August 2012.

Information about bank accounting, default mechanics, and regulatory treatment changes over time. This post simplifies bank balance sheet accounting for explanatory purposes. Real bank financial statements include many additional items (provisions, capital, RWAs, etc.) not covered here. Linked content may move or be updated without notice. This article is general information and analysis only and is not financial, accounting, or legal advice. Please verify the primary sources for yourself — that is half the point.