Why Your Grandfather Lived Off His Savings And You Cannot

Your grandfather retired on $500,000 in savings. He never touched the principal. The interest paid him enough to live on, take a holiday once a year, and leave the lot to your parents when he died.

You will not retire that way. Not because you saved less — adjusted for everything, plenty of people your age have done as well. You will not retire that way because the deal the bank offered him is not the deal the bank offers you. The same $500,000 today would pay you a small fraction of what it paid him, and you would eat into the principal to live.

This is not boomers winning a lottery. This is a structural change in what banks need from depositors — a change that unfolded across every developed economy between roughly 1971 and the late 1990s, under a single global wave of financial deregulation. If you’ve read Money From Nothing, The Cup Of Water, and What The Bank’s Credit Card “Risk” Actually Is, you already have the mechanism. This post is what the mechanism did to your grandfather’s retirement, and to your future one.

The Deal Was Not Different — The Brakes Were

One thing to clear up before the story works.

The bank’s ability to create money from nothing did not begin in the 1980s. The mechanism — a loan brings a matching deposit into existence by keystroke — has been the legal architecture of every chartered commercial bank since the Bank of England’s 1694 royal charter. Your grandfather’s bank in 1965 was, technically, doing the same thing your bank does in 2025. It was creating new money every time it wrote a loan.

What was different was not the mechanism. What was different was the brakes.

For most of the post-war era — roughly 1945 to the mid-1970s — every developed economy held bank credit creation in check through a stack of regulatory constraints:

- Reserve requirements — banks had to hold a substantial fraction of deposits as cash with the central bank, limiting how much new credit they could write against each deposit dollar.

- Interest rate ceilings — Regulation Q in the United States, similar regimes in the UK, Canada, Australia, France, Germany and Japan, set legal caps and floors on deposit and lending rates. Banks could not compete with each other into the floor; they had to compete for savers at fixed rates.

- Capital controls — cross-border movement of money was tightly restricted. Banks could not fund themselves via wholesale offshore markets the way they do today.

- Restrictions on what banks could lend on — some countries restricted what banks could lend into property, into equities, into consumer finance.

- The gold standard’s residue — until the 1971 closure of the gold window, central banks were ultimately constrained by their gold reserves, which throttled the whole system upstream.

Together these brakes meant that in 1965 a commercial bank’s lending was, in practice, limited by how much money it could attract from real savers. Banks had to compete for deposits. They advertised. They sent representatives to retiree golf clubs. They offered term deposits at rates designed to pull money in.

The wave that swept those brakes away ran roughly from 1971 to the late 1990s, in every developed economy, under different domestic political banners but always the same direction. It is the single most consequential financial-policy shift of the late twentieth century — and almost nobody alive today remembers life on the other side of it.

The Wave That Took The Brakes Off — By Country

A single thirty-year wave. The same direction in every developed economy. The brakes off the same mechanism that had existed for three hundred years.

The Deal The Bank Once Offered Savers

Before the wave hit, a commercial bank in any developed economy — in 1965, in 1972, in much of the world still in the early 1980s — functioned in practice as something close to an intermediary. The textbook story was approximately true: the bank took deposits from savers, paid them interest, and lent that money to borrowers at a higher rate, keeping the spread.

If the bank ran short of deposits, it could not, in practice, make new loans — reserve requirements and interest rate ceilings forced it to attract real savings before extending real credit. Deposits were not yet a “byproduct” of lending; they were the raw material of lending.

This meant that banks had to compete for deposits. They advertised. They sent people to talk to retirees at golf clubs. They offered term deposit rates that were attractive — high enough to draw money in.

In the United States in 1980, a six-month CD paid around 13%. Inflation was around 11%. The real return on cash savings was positive. In Australia in 1985, a one-year term deposit paid around 12%, against inflation of roughly 7–8% — a real return of 4–5%. In the United Kingdom in 1985, building society deposit rates ran 9–10% against inflation of 6%. In Canada, Germany, the Netherlands, and most of the OECD in the early 1980s the picture was the same: deposit savers received a positive real return on cash. That was enough to live on, if you had saved enough.

A retiree with $500,000 of saved labour, sitting in a term deposit at the rates that prevailed before the wave finished, was paid roughly $50,000–$60,000 a year just to keep it there. That paid for food, the house, the holiday, and the discretionary. The principal stayed intact. The children inherited the principal, often plus more, when the retiree died.

That is what “living off your savings” used to mean. It was the normal, expected, designed outcome of saving for forty years — not a feature of any particular country, but of an entire regulatory regime that the wave then dismantled.

The Deal The Bank Offers You

The bank today does not need your deposit.

When a borrower walks in for a loan, the bank does not check whether enough savers have come in to fund it. The bank types the loan into existence. The mechanism is the one the Bank of England documented in their 2014 paper — a loan creates a deposit, not the other way around. The bank’s lending capacity is constrained by capital requirements (calibrated by national prudential regulators) and demand from borrowers — not by the supply of savers’ deposits.

Crucially, the bank can also fund itself through wholesale money markets, central bank repo windows, securitisation pipelines, and offshore funding lines — all of which were unavailable or tightly capped before the wave. Deposits are now one of several funding sources, and not the cheapest after central bank quantitative-easing programmes pushed the cost of wholesale funding through the floor.

Because the bank no longer needs your deposit to make loans, the bank no longer has to compete hard for it. The bank does still want your deposit — it lowers their funding costs slightly, and it gives them a low-cost float to invest. But “want” is not “need.” And the price of a thing the buyer wants but does not need is always low.

A term deposit rate in 2025 across most developed economies is in the 3–5% range. Inflation is roughly 3–4%. The real return is approximately zero. Sometimes negative.

The same $500,000, sitting in the same kind of product, at a bank operating under the same architecture — to fund a retirement — is now paying about $20,000 a year. Before tax. Before inflation. After inflation, in real terms, that’s a few thousand of actual purchasing power, if you’re lucky.

$20,000 a year does not pay for a retirement. Not in the United States, the United Kingdom, Canada, Australia, the eurozone, or anywhere else the wave has finished.

The Quiet Difference

Your grandfather’s bank had brakes on it. Your bank does not. So your bank does not have to pay for your savings.

The mechanism — loan-creates-deposit — is the same mechanism it was in 1694. What changed was the regulatory wave that removed the constraints on it across every developed economy between 1971 and 1999.

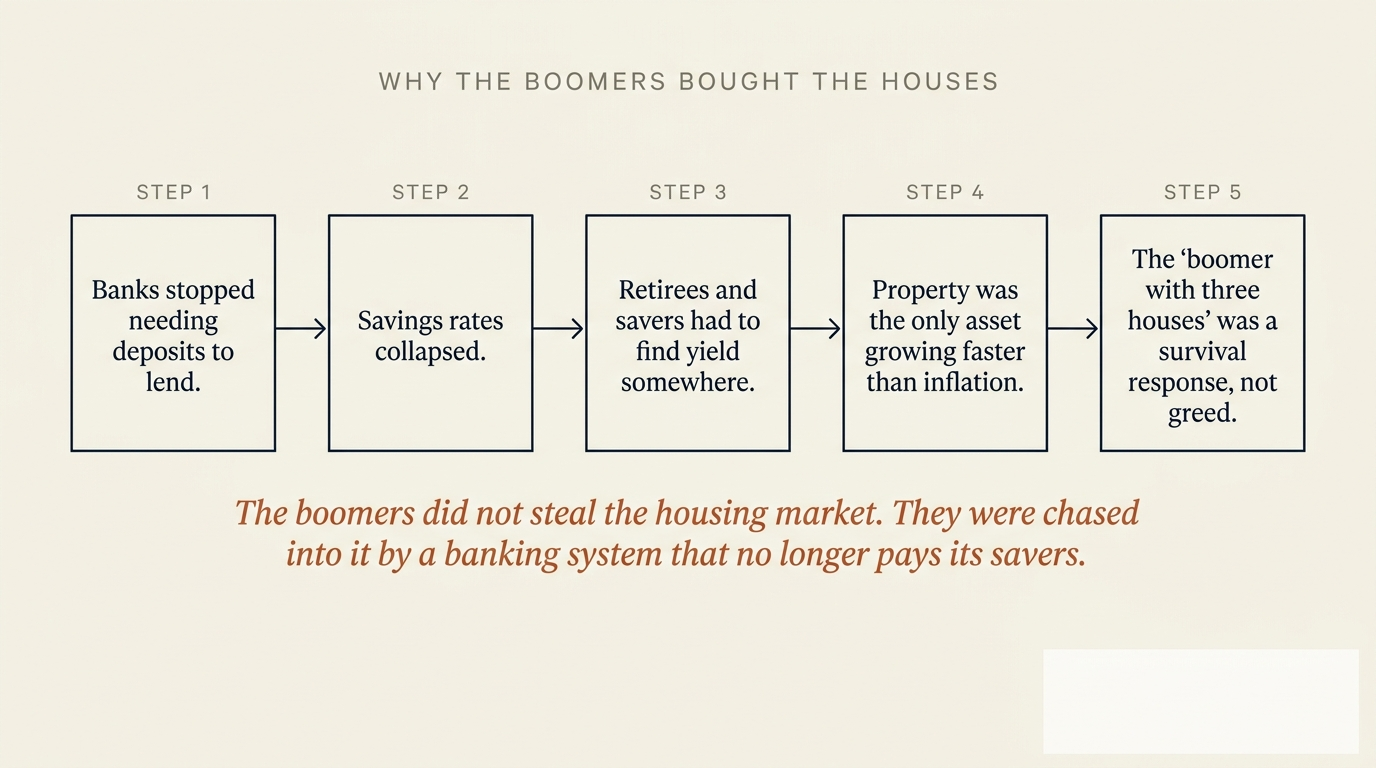

Why The Boomers Bought The Houses

This is where it gets uncomfortable for the generational discourse, because the boomers did not “steal” the housing market. They were chased into it by a banking system that stopped paying its savers.

Picture a retiree in 1995, anywhere in the developed world. They have $400,000 saved. The term deposit they relied on for the past decade has just dropped from 10% to 6%. By 2000 it would drop to 5%. By 2010 to 3%. By 2020 to under 1%. By 2022 they were earning thirty dollars a year per $10,000 saved.

What do they do? They cannot live on it. So they look around for an asset that grows.

The asset that obviously grew, year after year, was residential property — in every developed economy. Real house prices in the United States rose roughly 70% between 1985 and 2007. In the United Kingdom they roughly tripled. In Australia they roughly quadrupled. In Canada they doubled. In the Netherlands and Spain they tripled. The same shape, the same direction, the same period — fuelled, we now know, by the very same bank credit creation that had made the retiree’s savings useless.

So the retiree sold the savings out of the term deposit, put a deposit down on an investment property, took out a mortgage — at a much lower rate than the bank now charges them, because they were a high-quality borrower — and the rent paid the mortgage, and the property went up.

Then they did it again with the next $200,000 they could lay hands on.

By the time the same retiree was 75, they owned three houses. Their children’s generation could not afford one.

This is not a defence of every behaviour exhibited by every boomer. Some boomers are arseholes. So are some millennials. The point is structural. The boomer-with-three-houses outcome is partly a downstream consequence of the bank’s switch from constrained intermediary to unconstrained creator — the same switch that made the boomer’s savings stop paying.

The young person looking at the boomer with three houses and feeling priced out is not wrong about being priced out. They are wrong about who priced them out. It was not the boomer. It was the banking licence that paid the boomer’s savings nothing and then funded the boomer’s property purchase at low cost. The same banking licence, in every country.

The boomers did not steal the housing market. They were chased into it by a banking system that no longer pays its savers.

— The single sentence the generational discourse should turn on.

Who Won, Who Lost, Across Two Generations

A Quiet Invitation

If the generational discourse just shifted for you, the next post should land in your inbox.

What The Wave Actually Did To The Saver

The cleanest summary of the consequence, against the cleanest summary of the cause:

What This Means If You Are Saving Today

If you have saved diligently — working extra hours, putting money into a bank account, and watching it earn essentially nothing — you are not doing it wrong. The system is doing it to you. The mechanism that took your grandfather’s deal away is the same mechanism that means the next forty years of saving will not buy you what forty years of saving bought him.

This blog is not in the personal-finance business. What you do with your own savings is between you and a fee-only adviser whose interests are not tied to a product sale. The observation is structural: in the current architecture, cash sitting in a bank account loses real purchasing power most years, by design, in every developed economy.

The right answer to that observation is not “be cleverer with your savings.” The right answer is to change the architecture.

The Chicago Plan, the Vollgeld referendum, sovereign money — all of them propose returning banks to the constrained intermediary role they had before the wave. Under those proposals, banks would again need real savings to lend. They would again have to compete for deposits. Savings rates would return to something resembling a positive real return. The constructive arm of this blog covers those proposals in detail — see In 2018 The Swiss Almost Banned Bank Money Creation. None are mystical. All have been seriously argued by mainstream economists.

Three Questions Everyone Should Ask

The savings-rate collapse is built to make these three questions impossible to dodge.

Get The Next Post By Email

One plain-English post at a time. No tracking pixels. No advertising. Unsubscribe in one click. Your email goes to [email protected] and nowhere else.

Have you noticed yet?

Frequently Asked Questions

Hang on — were banks really not creating money in 1965? You said earlier they have been since 1694.

Correct — they were creating money in 1965, and they have been since 1694. The point of this post is that the mechanism has been there the whole time, but the constraints on the mechanism were strong in the post-war decades and were progressively removed between 1971 and 1999. Pre-wave: banks created money but were constrained by reserve requirements, rate ceilings, and capital controls to the point where they had to compete for real depositors. Post-wave: the constraints are gone and they don’t. Same mechanism, different brakes.

Weren’t 1980s interest rates high just because of high inflation?

Partly. The nominal rate was inflated by the inflation environment. But the real return on savings — nominal minus inflation — was still around 4–5% in most developed economies in the mid-1980s, which is a positive real return. Today’s real return on cash is roughly zero. The point holds.

Don’t mandatory retirement-savings accounts solve the problem?

Mandatory pension schemes — superannuation in Australia, 401(k) plans in the United States, ISAs and SIPPs in the United Kingdom, RRSPs in Canada, pension pillars in the eurozone — are a partial response, not a structural solution. They force savings into asset-price-inflated markets (property, listed equity) — the same markets the credit-creation system has been inflating. They are also subject to substantial management fees that, compounded over a working life, materially erode the balance. They mitigate the symptom; they do not fix the cause.

Isn’t it boomers’ fault they bought all the houses though?

Some boomers behaved opportunistically; that’s true of every generation. But the system’s design steered them. Central banks lowered policy rates throughout the 1990s and 2000s across every developed economy; savings products paid less and less; investment property became the rational alternative for anyone trying to maintain a retirement. The result is a structural outcome, not a moral one.

What about tax-deductible mortgage interest on investment property — isn’t that the real cause?

Tax-deductible interest on investment property — under different national names: “negative gearing” in Australia, mortgage interest deduction in the United States, similar regimes in the Netherlands and Sweden — accelerates the problem but doesn’t cause it. Even with no tax deductibility, a system in which savings pay nothing and credit creation fuels property prices would produce similar generational asset concentration. The tax break turns up the dial on a process the credit-creation system already started.

Would sovereign money restore the savings deal?

Yes, structurally. Under sovereign money proposals — Chicago Plan, Vollgeld, Sigurjónsson Report, NEED Act — banks become constrained intermediaries again. They would need real savings to lend. They would have to compete for deposits. Savings rates would return to something resembling a real return. That is precisely why those proposals are buried by the banking lobby every time they surface in any country.

About The Author

M. Notice

M. Notice writes NoticedYet, a calm, sourced blog about how private commercial banks create money out of nothing and what that means for the rest of us. The pen name is a voice choice, not opsec. Every post is primary-source-anchored. No products endorsed. No politicians backed.

Reach out: [email protected]

Sources

- McLeay, Radia, Thomas. “Money creation in the modern economy.” Bank of England Quarterly Bulletin, Q1 2014.

- Bank for International Settlements. Working Papers on financial deregulation and credit expansion in the 1980s and 1990s.

- Federal Reserve Economic Data (FRED). Three-month interbank rates, historical series for OECD economies.

- European Central Bank. Bank interest rate statistics — eurozone deposit rate history.

- Benes, Kumhof. “The Chicago Plan Revisited.” IMF Working Paper WP/12/202, August 2012.

- Bank for International Settlements. Residential property price statistics — long-run series across reporting jurisdictions.

- Joseph Huber. Sovereign Money: Beyond Reserve Banking. Palgrave Macmillan, 2017.

- Wikipedia. “Big Bang (financial markets)” — overview of the 1986 UK deregulation and the wider 1980s wave.

Disclaimer

The numerical examples are illustrative, drawn from typical deposit and inflation rates across developed economies in the relevant decades. Actual rates vary by country and product. Linked content may move or be updated without notice. This article is general structural analysis only and is not financial, tax or pension advice. Please verify the primary sources for yourself — that is half the point.