In 2018 The Swiss Almost Banned Bank Money Creation

On 10 June 2018, the Swiss electorate voted on a constitutional amendment that would have ended private commercial bank money creation. The proposal was called the Vollgeld-Initiative — “full money,” “sovereign money.” If passed, it would have made Switzerland the first country in the modern era to constitutionally restore money creation as a public function bound by formula.

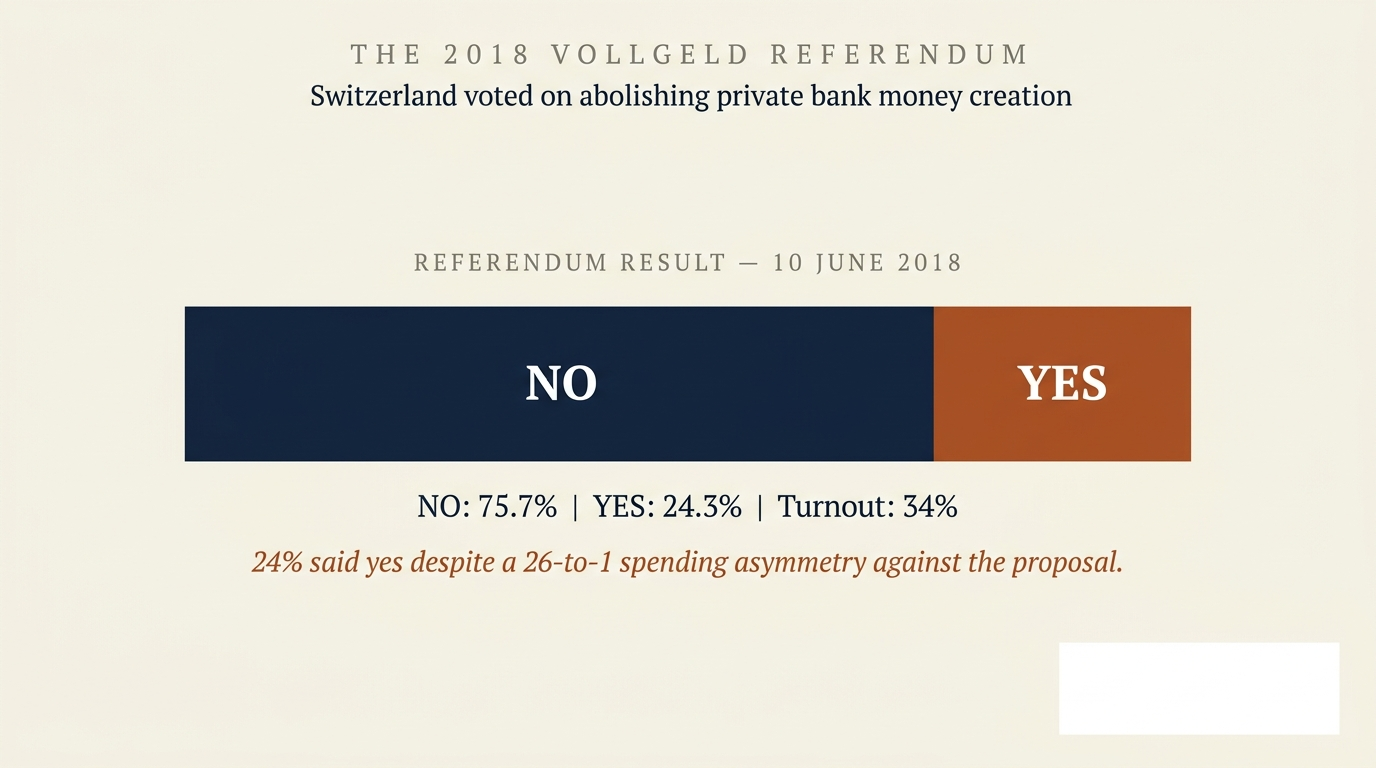

It did not pass. The vote was 75.7% no, 24.3% yes. Switzerland kept its current banking system.

That is the headline. The full story is the most encouraging piece of evidence in modern banking-reform politics. This is the closing post of the NoticedYet launch corpus. It builds on every post that has come before it — Money From Nothing, The Cup Of Water, What The Bank’s Credit Card “Risk” Actually Is, Why Your Grandfather Lived Off His Savings And You Cannot, Buying Your Hard-Built Business With Conjured Money, If You Do Not Repay, Who Actually Loses?, Where The First $380,000 Of Your Mortgage Payments Actually Go, The Real Heist Movie Has Not Been Made Yet, and But Will We End Up Like Zimbabwe?. It says: there is an alternative. There has always been an alternative. People who have looked at the system clearly have proposed it for almost a century. In 2018, one developed country came close to adopting it.

What Vollgeld Was

The proposal sat alongside one constitutional amendment that would have, in plain terms:

- Made the Swiss National Bank the sole issuer of money. Both physical cash and electronic deposit money. No exceptions.

- Made commercial banks into true intermediaries. Banks could lend only money they actually held. The deposit-creation mechanism we have been documenting on this blog — loans creating deposits, deposits funding nothing — would have been abolished.

- Distributed new money debt-free. When the SNB issued new money to keep the supply in line with economic growth, it would have been transferred to the federal government (for general spending), to the cantons, or directly to citizens as a “citizen dividend.”

- Returned seigniorage to the public. The profit from money creation — currently captured privately by commercial banks — would have flowed to Swiss citizens.

This is the cleanest constitutional money-reform proposal ever put to a national vote. The drafting was rigorous. It was developed over a decade by the Verein Monetäre Modernisierung (MoMo, the Swiss “Monetary Modernisation Association”), building on the theoretical work of Joseph Huber, the German economist whose 2017 book Sovereign Money: Beyond Reserve Banking is the standard modern text on the system.

The Vote, And What It Actually Showed

The vote was, on its face, decisive. 75.7% no, 24.3% yes. In Swiss political terms that is a substantial defeat.

The interesting figures are the ones underneath. Look at how the campaign was actually fought.

Spending asymmetry: approximately 26 to 1. The “no” campaign, funded by Swiss commercial banks, business federations, the Swiss National Bank, and the federal government, spent an estimated CHF 6,500,000 against the proposal. The “yes” campaign, funded by small donations to MoMo, spent an estimated CHF 250,000 for it.

Establishment alignment: total. Every major Swiss bank opposed it. The Swiss National Bank chairman publicly called it “dangerous.” Every major political party except a fringe minority opposed it. Every major Swiss newspaper editorialised against it. Most “expert” commentary in mainstream media presented only the “no” arguments.

Public education on the proposal: essentially zero. Most Swiss voters first heard about Vollgeld in the months immediately before the vote. There had been no sustained public education tradition, no mainstream press coverage, no school curriculum. The proposal arrived in the public consciousness almost cold.

Under those conditions, 24% of Swiss voters said yes.

That 24% is the most interesting number in modern banking-reform politics. It is the natural floor of public understanding under maximum hostile conditions. It is the share of voters who could figure out, in months, against an avalanche of “no” messaging, that the proposal was correct enough to vote for. Under conditions of sustained public education over years, the floor would have been higher. Under any balanced media environment, the floor would have been considerably higher.

For comparison, the 24% Vollgeld result is roughly twice the share of voters who routinely support major Swiss left-wing initiatives. It is comparable to the size of the Swiss libertarian or anti-EU constituencies on questions where those movements have spent decades organising. Vollgeld got that level of support on a technical-banking-reform question with three months of campaigning and a 26-to-1 spending disadvantage.

The Bedrock Signal

Twenty-four percent of Swiss voters said yes to constitutionally abolishing private bank money creation. Against the entire establishment. With three months of organising.

That is the floor, not the ceiling. With sustained public education over years, the floor becomes the foundation. The next 25% — the voters currently scared by establishment messaging — are reachable.

This Is Not A Fringe Idea

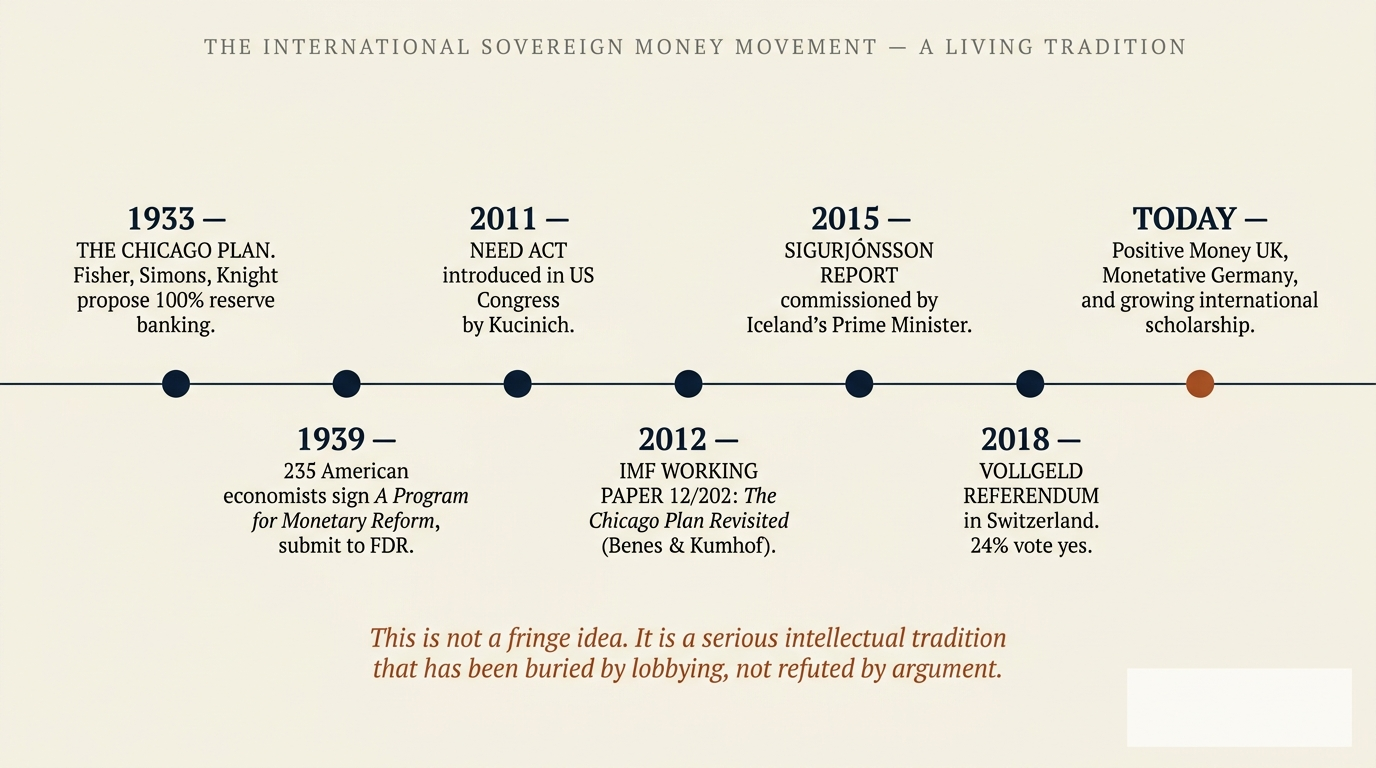

The Vollgeld initiative is the most recent national-vote landmark in a much longer intellectual tradition. The full story is worth knowing.

1933 — The Chicago Plan. Three University of Chicago economists — Irving Fisher, Henry Simons and Frank Knight — published A Program for Monetary Reform. The proposal: end commercial bank money creation, require 100% reserves on deposits, make the central bank the sole money issuer. Fisher was one of the most influential American economists of the era. Knight was the founder of what became the “Chicago school.” The proposal was not fringe; it was central.

1939 — A formal submission to FDR. The Chicago Plan was refined and signed by 235 American economists. The proposal was submitted to President Franklin D. Roosevelt. He read it. He did not act on it. The banking lobby made sure it stayed buried during the wartime preparations.

2011 — The NEED Act in US Congress. Dennis Kucinich introduced the National Emergency Employment Defense Act (HR 2990). Drafted by the American Monetary Institute (Stephen Zarlenga’s organisation). Would have abolished the Federal Reserve as a private institution, transferred money creation to the US Treasury, ended fractional reserve banking. Did not pass. Was buried in committee.

2012 — The IMF working paper. Jaromir Benes and Michael Kumhof, two IMF economists, published The Chicago Plan Revisited as IMF Working Paper WP/12/202. They ran the Chicago Plan through modern computational economic models. Their conclusion: government debt could be paid down to near zero, financial crises virtually eliminated, output could rise by approximately 10%. The paper sits on the IMF’s own website. The mainstream financial press did not cover it.

2015 — The Sigurjónsson Report in Iceland. Iceland’s Prime Minister commissioned Frosti Sigurjónsson, a member of Parliament, to study sovereign money reform. The resulting report concluded that fractional reserve banking was the cause of Iceland’s repeated financial crises. It recommended sovereign money reform. The banking lobby pressed back. The report was shelved but is still publicly available.

2018 — Vollgeld. Switzerland’s national vote. The first time a developed economy’s voters were asked directly. 24% said yes despite everything.

Today. Positive Money in the UK has detailed legislative drafts, briefs UK Parliament, and runs sustained public education. Monetative in Germany is Joseph Huber’s theoretical home. The American Monetary Institute continues in the US. Sovereign Money Network coordinates internationally. The movement is small but serious, well-documented, intellectually rigorous, and has yet to be defeated on argument.

A Quiet Invitation

If this is the first time you have seen the international sovereign-money tradition laid out in one place, get the next post in your inbox.

What Would A Vollgeld-Style Reform Look Like In Australia?

The mechanics would be straightforward enough to draft. The political work would be the harder problem — but the political work can be done.

A draft Australian Vollgeld-equivalent would include:

- Constitutional clause. Sole authority to create currency vested in a public authority — possibly an expanded Reserve Bank under new constraints, possibly a new entity. The authority’s annual issuance is bound by a formula tied to verifiable economic indicators (GDP growth, productivity, population, or a commodity reserve).

- Abolition of commercial bank credit creation. Banks lose the right to create deposits through lending. Banks lend only saved deposits, becoming true intermediaries. This is the heart of the proposal.

- Transition mechanism. A staged conversion of existing bank-created deposit money to sovereign-issued money, over (say) ten years, with corresponding paydown of public debt funded by the conversion seigniorage.

- Citizen dividend. New annual issuance, where consistent with the formula, distributed partly to general government revenue and partly directly to citizens as an annual sovereign-money dividend.

- Audit and transparency. Quarterly public audit of the money authority’s operations. Open data.

- Referendum trigger to amend. The formula and the authority’s mandate can only be changed by national referendum, not by parliamentary majority.

The IMF’s 2012 modelling suggests this would, in addition to ending private seigniorage capture: pay down most of the federal debt over time, reduce financial crisis frequency by an order of magnitude, increase real economic output by approximately 10% in the long run, and stabilise inflation.

It would also, critically, restore real returns to savers. Banks would have to compete for deposits again. The world your grandfather lived in — where savings paid a real return and you could retire on a sensible balance — would be possible again.

Australian housing prices would settle to what real saved capital could support, rather than what infinite bank credit can stretch to. The grandchildren currently locked out of the housing market would not stay locked out.

This is not a fringe idea. It is a serious intellectual tradition that has been buried by lobbying, not refuted by argument. There is an alternative. Twenty-four percent of Swiss voters could see it in three months. Tens of millions of others can see it given time.

— The closing sentence of the NoticedYet launch corpus.

The Long Game

The Vollgeld result is read by some reform advocates as a defeat. NoticedYet reads it as a signal.

The 24% bedrock was earned under conditions you could not engineer to be worse: no public education, three months of campaigning, every establishment institution against, a 26-to-1 spending asymmetry. The fact that one-quarter of voters figured it out anyway is not a defeat. It is a glimpse of what the conversation could be under fair conditions.

The mainstream press will not give the conversation fair conditions. The banks fund too much of mainstream media. The political class is captured. The educational curriculum is silent. The “experts” are mostly bank-adjacent.

What sustains the movement is sustained public education by writers, researchers, organisers, and ordinary curious citizens who have decided to learn the mechanism for themselves. Over years, that adds up. By the time the next national vote on sovereign money happens — somewhere, in some developed country — the bedrock could be 30%, 40%, or higher. At those levels, the campaign asymmetry no longer holds.

NoticedYet exists to be one drop of that long, slow education project.

If you have read this far, you are now part of it.

Three Questions Everyone Should Ask

The Vollgeld story makes these three questions impossible to dodge.

Get The Next Post By Email

One plain-English post at a time. No tracking pixels. No advertising. Unsubscribe in one click. Your email goes to [email protected] and nowhere else.

Have you noticed yet?

Frequently Asked Questions

Why did Vollgeld lose if the case was so strong?

Three reasons. First, three months of campaigning is not enough to overcome decades of silence. Most voters had not heard of the proposal until weeks before the vote. Second, the 26-to-1 spending asymmetry meant most voters encountered only “no” messaging. Third, mainstream media framed the proposal as risky and untested, which was technically accurate (it has not been tried) but obscured that no proposal has been tested without first surviving public adoption.

Would the citizen dividend cause inflation?

Not under the Vollgeld design. The total money supply expansion in a year is set by formula based on real economic indicators. Whether that expansion is distributed through government spending, via citizen dividend, or both is a distributional question, not an inflationary one. The total amount of new money is fixed by the rule, not by political demand.

What happens to existing bank loans during the transition?

The proposed transition mechanisms typically gradually convert existing deposit money to sovereign money over a decade, with corresponding paydown of public debt. Existing loans continue to operate; banks become true intermediaries going forward, lending only what they actually hold. The proposals are usually backward-compatible with existing contracts.

Wouldn’t banks just leave for jurisdictions without sovereign money?

Some would, in the short run. Many would not, because banking under a sovereign money system remains a profitable, legitimate intermediary business. The Swiss banking sector was strongly opposed to Vollgeld precisely because it would have abolished the most profitable part of banking — not because it would have ended banking. There is a profitable bank under sovereign money. It just is not the bank we currently have.

Is there a realistic Australian path to sovereign money?

Realistic in the long run. Not in the next election. Australia’s path would likely follow the same pattern as Switzerland’s — years of public education, gradual mainstream acceptance, eventual constitutional referendum. The Australian Constitution can be amended by referendum. The bar is high (double majority requirement). The proposal would need significant public support before being put to a referendum. This blog exists in part to contribute to that public education.

What can I do to help?

Read further. The international sovereign money movement has substantial primary literature; the Vollgeld and Positive Money websites are excellent starting points. Talk to people you know about the mechanism. Subscribe to this blog or other primary-source-anchored writing on monetary reform. Long-game civic education is the work; everyone who participates moves the needle slightly. The bedrock floor of public understanding rises over decades, one informed citizen at a time.

About The Author

M. Notice

M. Notice writes NoticedYet, a calm, sourced blog about how private commercial banks create money out of nothing and what that means for the rest of us. The pen name is a voice choice, not opsec. Every post is primary-source-anchored. No products endorsed. No politicians backed.

Reach out: [email protected]

Sources

- Verein Monetäre Modernisierung (MoMo). The official Vollgeld-Initiative website and source documentation.

- Benes, Kumhof. “The Chicago Plan Revisited.” IMF Working Paper WP/12/202, August 2012.

- McLeay, Radia, Thomas. “Money creation in the modern economy.” Bank of England Quarterly Bulletin, Q1 2014.

- Positive Money UK. Sovereign money campaign, legislative drafts, and detailed policy papers.

- Joseph Huber. Sovereign Money: Beyond Reserve Banking. Palgrave Macmillan, 2017 — the standard modern text.

- Sigurjónsson Report (Iceland 2015) — sovereign money reform commissioned by Iceland’s Prime Minister.

- Monetative (Germany) — Joseph Huber’s German sovereign money organisation.

Information about international sovereign money proposals and the Vollgeld initiative is drawn from published primary sources. Vote percentages are official Swiss federal data. Campaign spending estimates are widely cited but methodologically debated; the order of magnitude is not in dispute. Linked content may move or be updated without notice. This article is general information and analysis only and is not financial, economic, or legal advice. Please verify the primary sources for yourself — that is half the point.