Where The First 380000 Of Your Mortgage Payments Actually Go

A borrower in any developed economy takes out a $600,000 mortgage. They pay roughly $3,600 a month for the next ten years. By the end of that decade, they have handed their bank $432,000 of real, earned money. They sit down to check the loan balance.

It has gone down by $100,000.

The other $332,000 went to the bank. It was earned through real labour. It is no longer in the borrower’s account. It is the bank’s. The bank’s economic cost to issue the loan in the first place was zero — the principal was created by typing a number into a screen on the day of settlement (see Money From Nothing for the mechanism).

This is the standard 30-year fully-amortising fixed-payment mortgage. It is the dominant home-loan product in the United States, the United Kingdom, Canada, Australia, New Zealand, Ireland, much of continental Europe, and most Asian and Latin American economies. Almost nobody understands how aggressively it is stacked toward the bank in the early years — or that the stacking is deliberate. This post shows the machine. It builds on The Cup Of Water, What The Bank’s Credit Card “Risk” Actually Is, Why Your Grandfather Lived Off His Savings And You Cannot, Buying Your Hard-Built Business With Conjured Money, and If You Do Not Repay, Who Actually Loses?. If you’ve read those, the mortgage maths becomes a different conversation entirely.

What Year One Of The Machine Actually Does

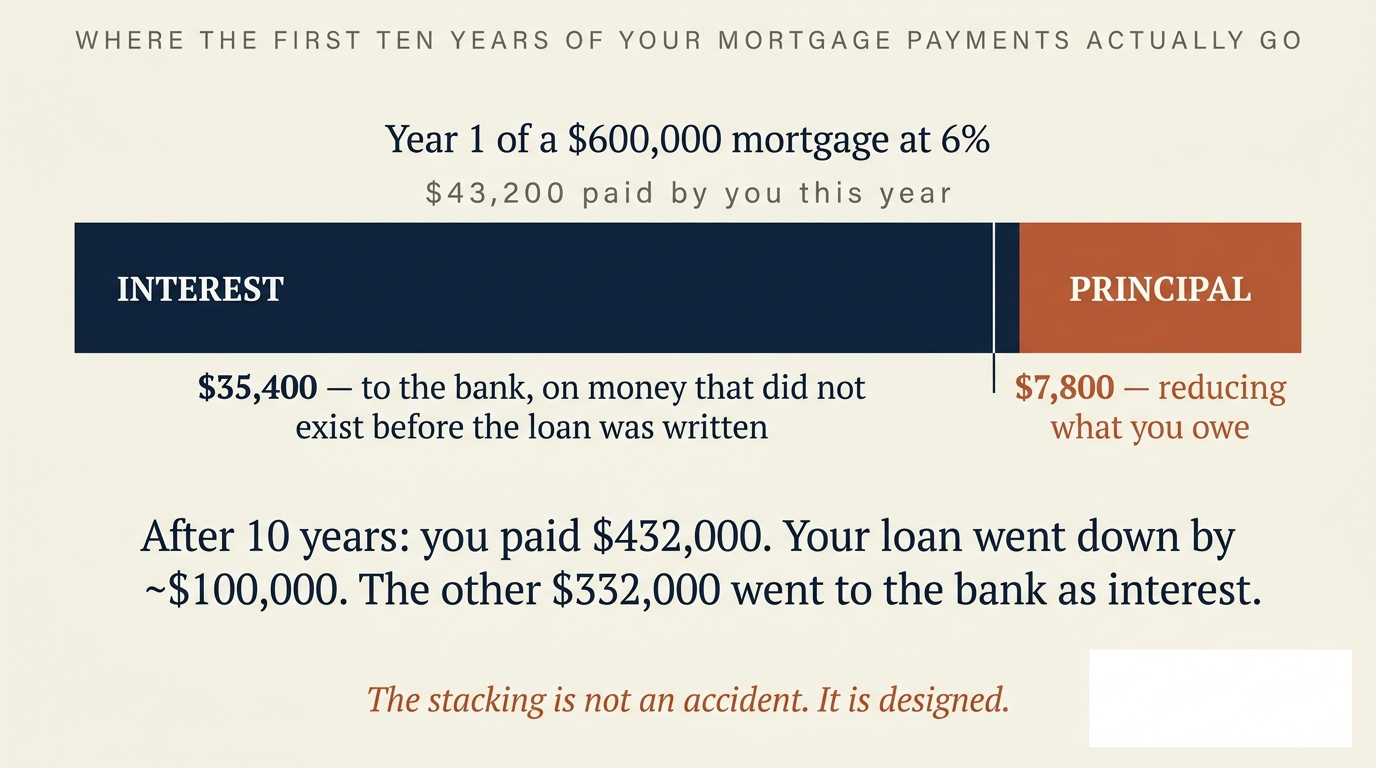

Take the standard parameters. $600,000 borrowed, 30 years, 6% interest rate. The fixed monthly payment is roughly $3,600. Total over the first year: $43,200.

Of that $43,200, the bank takes:

- Interest: $35,400 (about 82% of what the borrower paid)

- Principal reduction: $7,800 (about 18% of what the borrower paid)

The borrower worked real hours, paid real tax, and handed over $43,200 of after-tax money. Of that, the bank took $35,400 as interest on money the bank typed into existence on the day of settlement. The remaining $7,800 actually shrank what the borrower owed.

Year two is barely different. The principal portion creeps up to about $8,300 because the balance is now slightly smaller. By year three, it’s $8,800. The curve is shallow on purpose — the bank’s harvesting window has 25 more years to run.

By year ten, the borrower has paid $432,000 in total. Their balance has dropped by about $100,000. The bank has captured $332,000 of real labour as profit on a loan it created from nothing.

The borrower “owns half their home” in the sense that they’ve been paying for a decade. Mathematically, the bank owns five-sixths of what they’ve paid.

The Harvest: First Decade

The borrower pays $432,000 in the first decade. The loan shrinks by about $100,000. The remaining $332,000 is the bank’s.

All of it is interest charged on money the bank invented when the loan was signed. The bank’s economic cost to create that money: zero.

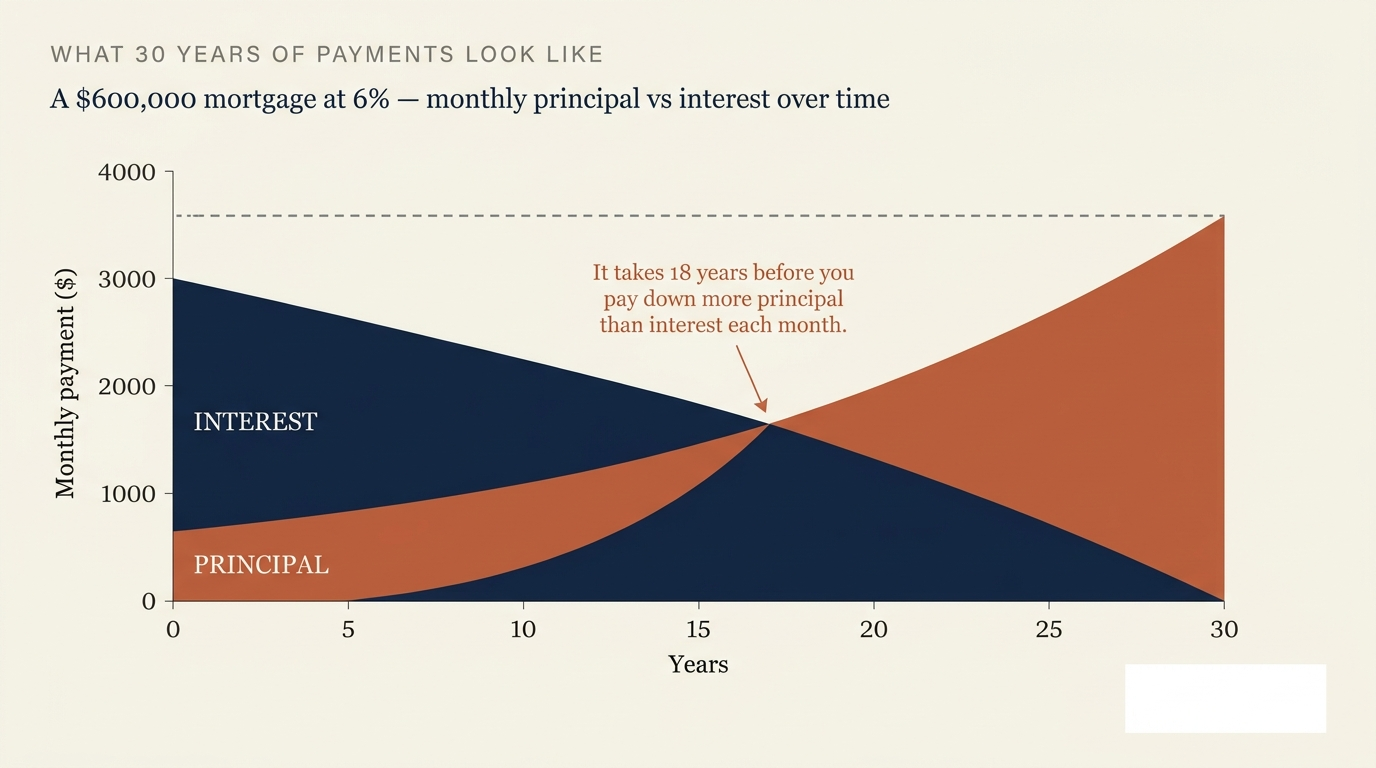

What 30 Years Looks Like

The full 30-year curve makes the harvesting design visible. The total monthly payment is constant at around $3,600. What changes month to month is the split.

In month one, the bank takes 83 cents of every dollar.

By month 60 (year five), the bank’s share has dropped to 75 cents.

By month 120 (year ten), the bank’s share is 63 cents.

By month 216 (year 18 — the crossover), the borrower finally hands over more money to their own equity than to the bank.

By month 360 (year 30), the bank is taking near-zero. The harvest is over — for that loan.

Over the full 30 years, the borrower pays about $1.29 million in total:

- $600,000 of principal repayment — returning the conjured loan amount

- $690,000 of interest — pure profit to the bank, on money it created from nothing

The bank lent the borrower nothing real. The bank received $690,000 of real labour over thirty years. The bank’s operating cost to handle the loan was perhaps $20,000 in real expense. The remaining $670,000 is the economic margin on the act of typing a number into a screen.

Why The Stacking Is Designed This Way

Three structural reasons. Each tilts the harvest further toward the bank.

One. Interest accrues on the outstanding balance. Interest is calculated each month on whatever is currently owed. In month one, the balance is the full $600,000, so interest is large. By month 360, the balance is near zero, so interest is tiny. This is arithmetic, not a trick. The bank did not invent the math. But the math means any loan structure is, by default, front-loaded with interest — and the bank chose the loan structure.

Two. The fixed monthly payment is engineered to amortise to zero over the term. The payment is set just large enough that, by the end of 30 years, the principal has been fully repaid. This means in the early years — the years when interest is largest — the payment barely touches the principal. The architecture maximises interest capture in the period during which most borrowers will not be on this loan anymore (see below).

Alternative payment structures exist mathematically. An “even principal” structure would have the borrower pay $1,667 of principal every month consistently, with declining interest on top. Early payments would be larger (when most borrowers can least afford them); late payments would be smaller. Total interest over the life of the loan would be a third lower. Banks across the developed world do not offer these as the default product. The 30-year fully-amortising fixed-payment mortgage is dominant because it maximises the bank’s interest capture in the period during which most borrowers refinance, sell, or default.

Three. The seven-year sweet spot. Across developed-economy mortgage markets — US, UK, Canada, Australia, Germany, the Netherlands — the average mortgage is held for roughly five to seven years before being refinanced, sold, or restructured. Look at what the bank has collected in the first seven years of a $600,000 mortgage at 6%: roughly $238,000 in interest, against only ~$60,000 of principal repaid. When the borrower refinances or sells, the loan is paid out at the still-near-original balance, and the bank books the full $238,000 of interest as profit.

If the borrower refinances into a new 30-year loan, the amortisation clock starts over. The next seven years extract another $238,000 of interest on the new loan. The bank’s interest capture is maximised by the borrower behaviour the mortgage market itself encourages through its product design.

A Quiet Invitation

If you’ve just noticed how the bank’s machine is engineered, you’re going to want the next one in your inbox.

The Perpetual Harvest: How Refinancing Resets The Bank’s Front-Load

Every refinance hands the bank a fresh 30-year extraction window.

When a borrower refinances, they start a new 30-year loan. The amortisation clock starts over. Years 1-7 of the new loan are front-loaded with interest the same way the original loan was, just at a slightly different rate.

If a borrower refinances after seven years of their original loan, they have already paid $238,000 in interest and only $60,000 in principal. The new loan starts at $540,000 (original balance minus the slim principal reduction). Over the next seven years of the new loan, the same pattern repeats. The bank captures another front-loaded interest stack.

Across a working life where the average borrower refinances every five to seven years, the cumulative interest paid is dramatically higher than what they would have paid if they had simply stayed on the original loan and let it amortise.

The “refinance to a lower rate” marketing is engineered to suggest that the new lower rate is the headline number that matters. The amortisation reset is the headline number nobody mentions. Lower headline rate, fresh interest harvest. The bank’s product structure does not require the borrower to do anything wrong — only to behave normally inside the harvesting machine.

Why Principal-First Mortgages Are Rare (And What That Tells You)

Mortgages that amortise principal-first — with higher early payments and lower late payments — cut total interest by roughly a third over the life of the loan. Mortgages with even-principal structures (constant principal reduction, declining interest on top) do the same. Mortgages on 15-year terms cut interest by close to half. All of these structures exist mathematically. None require new financial engineering. They could be the default product tomorrow.

They are not the default product. Across every developed economy, the 30-year fully-amortising fixed-payment mortgage is dominant. In the United States, the 30-year fixed is over 90% of new originations. In Canada, the 25-year amortisation is standard. In the United Kingdom, the 25-30 year repayment mortgage is the default product despite the typical interest rate being reset every 2-5 years (which functionally adds an interest reset to each rate period). In Germany, the Netherlands, and parts of Scandinavia, very long amortisations (sometimes 35-40 years) are the norm.

The market has converged on the product that maximises interest captured during the typical holding window. That convergence is not random. It is the equilibrium outcome of every bank optimising for the same target. Principal-first products are not banned. They simply are not marketed, not defaulted to, and not the structure that a first-time borrower constrained by house prices can actually afford. (House prices, in turn, are pushed upward by the same bank credit creation — see Why Your Grandfather Lived Off His Savings. The loop closes on itself.)

The product is engineered. The harvest is engineered. The borrower’s apparent freedom of choice is the choice between equivalent versions of the same machine, offered by every commercial bank in every developed economy.

The Same Machine, Every Country

Variations in payment structure. Same architectural principle. Same beneficiary class.

Three Questions Everyone Should Ask

The amortisation stacking is built to make these three questions impossible to dodge.

Get The Next Post By Email

One plain-English post at a time. No tracking pixels. No advertising. Unsubscribe in one click. Your email goes to [email protected] and nowhere else.

Have you noticed yet?

Frequently Asked Questions

Isn’t the amortisation just a function of compound interest? It’s mathematics, not a trick.

The arithmetic is unavoidable. What is not unavoidable is the choice to offer a 30-year fixed-payment fully-amortising mortgage as the default product in every developed economy. Alternative structures — shorter terms, principal-first, balloon-end, even-principal — all exist mathematically. The market has converged on the product that maximises interest captured during the typical holding period. That convergence across every country is not random.

If principal-first mortgages save borrowers a third of total interest, why don’t banks offer them as the default?

Because the bank’s profit on the loan would fall by roughly a third. Banks are publicly-listed companies optimising for shareholder return. The product that maximises shareholder return is the front-loaded 30-year mortgage. The product that minimises total interest extracted from the borrower would minimise the bank’s economic margin on the act of money creation. The two are the same trade-off seen from opposite ends.

Doesn’t the refinance market mean borrowers can shop around for better deals?

Every refinance restarts the amortisation clock at year zero. The new loan’s first decade extracts the same front-loaded interest the original did, just at a slightly different rate. The headline “lower rate” disguises a fresh interest harvest. Across a working life where the average borrower refinances every 5-7 years, cumulative interest paid is materially higher than simply holding the original loan to maturity. The refinance market is not the borrower’s escape route from the harvest — it is the harvest’s repeat cycle.

Why is this product the same in every developed economy?

Because the dominant beneficiary class is the same in every developed economy — the chartered commercial banking sector. The architecture of money creation that produced the harvest (see Money From Nothing) is the same architecture in every developed economy. The mortgage product is the downstream consequence of the same upstream system.

Would sovereign money change mortgage products?

Yes. Under sovereign money (see In 2018 The Swiss Almost Banned Bank Money Creation), banks would have to compete for real savers’ capital to fund mortgages. Real savers want their money back relatively soon. Mortgage products would shift toward shorter terms, lower loan-to-value ratios, and structures closer to the principal-first products that exist on the margin today. House prices would also fall to what the new credit conditions support, which would reduce the loan size a typical borrower needs.

Is this post telling me what to do with my own mortgage?

No. This blog is not in the personal-finance business. We show the architecture and the maths. What a reader does with their own mortgage is a matter for them and a fee-only adviser whose interests are not tied to a product sale. The point of this post is structural: the dominant mortgage product in every developed economy is engineered to maximise interest capture on money the bank created from nothing. That is a system-level fact, not an individual-borrower one.

About The Author

M. Notice

M. Notice writes NoticedYet, a calm, sourced blog about how private commercial banks create money out of nothing and what that means for the rest of us. The pen name is a voice choice, not opsec. Every post is primary-source-anchored. No products endorsed. No politicians backed.

Reach out: [email protected]

Sources

- McLeay, Radia, Thomas. “Money creation in the modern economy.” Bank of England Quarterly Bulletin, Q1 2014.

- Bank for International Settlements. Statistics on credit to households across reporting jurisdictions — mortgage credit aggregates.

- Federal Reserve Economic Data (FRED). 30-Year Fixed Rate Mortgage Average in the United States — historical rate series.

- European Central Bank. Bank interest rate statistics — housing-loan rates and terms across the eurozone.

- Benes, Kumhof. “The Chicago Plan Revisited.” IMF Working Paper WP/12/202, August 2012.

- Joseph Huber. Sovereign Money: Beyond Reserve Banking. Palgrave Macmillan, 2017.

Disclaimer

The numerical examples in this article are illustrative, calculated against the dominant 30-year fixed-payment fully-amortising mortgage in developed-economy markets. Actual rates, terms, and amortisation schedules vary by lender, country, and product. Linked content may move or be updated without notice. This article is general analysis of the structure of the mortgage market and is not financial, mortgage, or tax advice. Please verify the primary sources for yourself — that is half the point.