But Will We End Up Like Zimbabwe? No. Here Is Why.

Every time someone proposes ending private bank money creation, someone in the room says “but Zimbabwe.”

It’s a powerful scare. Wheelbarrows of cash. Billion-dollar notes. Bread queues. A government printing money until the currency became unusable. The image is vivid. It works.

It is also based on a misunderstanding of what actually happened in Zimbabwe, and the misunderstanding is doing load-bearing work in protecting the current banking system from reform.

This is one of the inoculation posts on NoticedYet. It builds on Money From Nothing, The Cup Of Water, and the other critique posts in the series. Its job is to dismantle the Zimbabwe scare before someone uses it on you.

The Standard Story

The standard version of the Zimbabwe story goes like this:

“Zimbabwe is what happens when government controls money. Robert Mugabe’s government decided to print money to pay civil servants, fund spending, and patronage. The central bank had no constraints. Hyperinflation followed. Therefore, any system that puts money creation under public control will end the same way.”

This story is so vivid, so emotionally available, and so well-rehearsed that it ends most banking-reform conversations within thirty seconds. It is also wrong at every level.

What Actually Happened In Zimbabwe

Zimbabwean hyperinflation, which peaked in 2008 at an estimated 89.7 sextillion percent month-over-month, was the product of five simultaneous failures, not one. The “government printed too much money” story is a one-failure narrative. Zimbabwe had five.

One. A collapsed productive economy. Between 2000 and 2003, the Mugabe government’s land reform programme destroyed commercial agriculture, the country’s largest export and food source. GDP fell by approximately 50% over 2000-2008. Less goods + same money supply = inflation. Less goods + expanding money supply = catastrophic inflation. The supply side was the central driver. Without the land-reform-induced economic collapse, the same monetary expansion would have produced bad inflation, not hyperinflation.

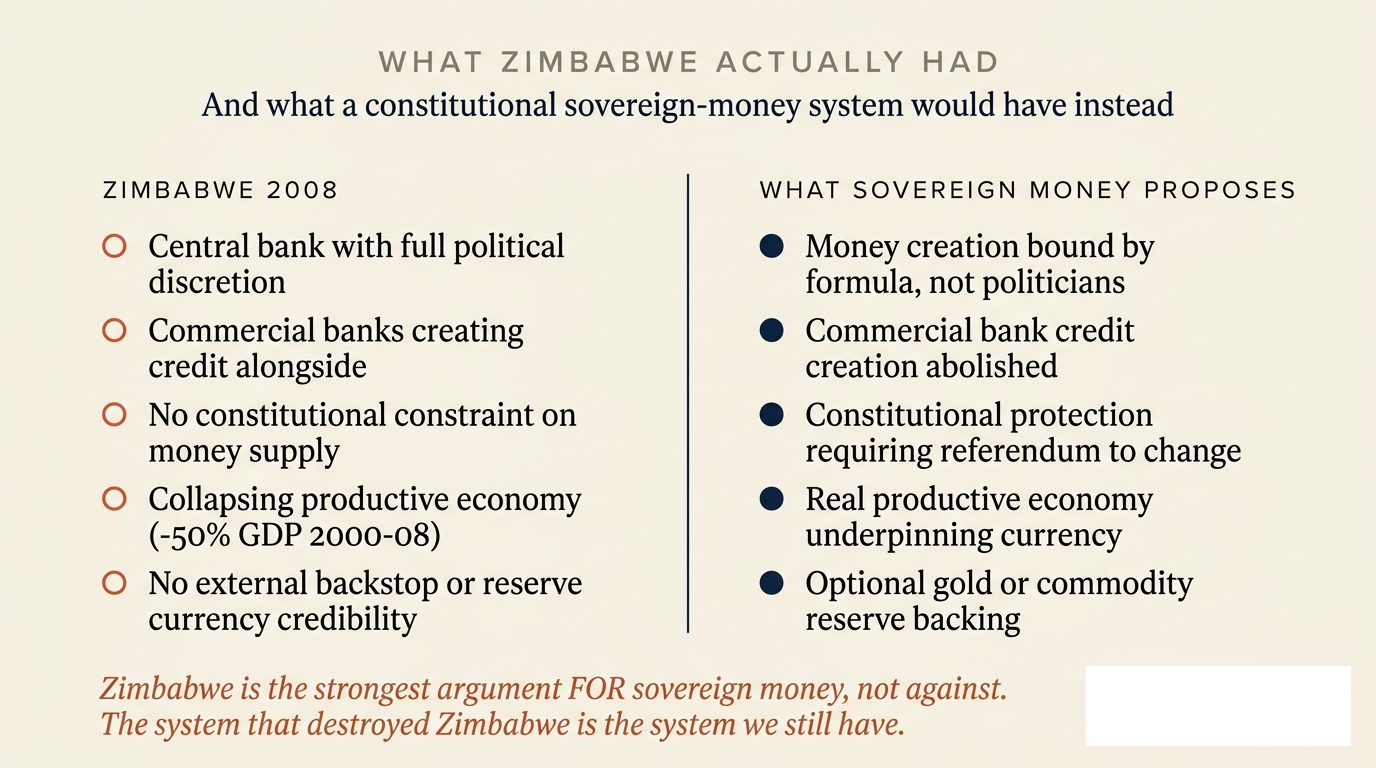

Two. A discretionary central bank captured by politics. The Reserve Bank of Zimbabwe had no constitutional or legislative constraint on its issuance. Under political pressure from the Mugabe regime, it expanded base money to finance government deficits, civil servant salaries, and patronage spending. The discretion was the problem, not “public control.” A public monetary authority bound by a formula would not have done what the RBZ did.

Three. Commercial banks creating credit alongside. Zimbabwe had a normal Western-style commercial banking system. Banks were creating credit through lending in the usual fractional-reserve way, on top of the central bank’s monetary expansion. Broad money grew at multiples of base money. This was NOT a sovereign money system. It was the current Western system operating under political collapse. Sovereign money proposals abolish commercial bank credit creation entirely.

Four. Political dysfunction. Capital controls failed. Foreign exchange manipulation. Expropriation of foreign-owned assets. Sanctions imposed by the United States and European Union. International withdrawal of investment. The state’s revenue base collapsed. The political choice became “print or fall.” Neither is a choice a properly designed monetary system should ever present.

Five. External isolation. No IMF facility. No reserve currency credibility. No external backstop. Anyone with USD or South African rand left the country. Currency flight accelerated the hyperinflation.

These five factors together produced what happened. Removing any one of them would have produced moderate-to-bad inflation, not hyperinflation. Removing the productive economy collapse alone would have prevented the catastrophe.

The Critical Point

Zimbabwe was NOT a sovereign money system. Zimbabwe was the current Western system — central bank + commercial bank credit creation — operating under political collapse.

Every sovereign money proposal (Chicago Plan 1933, IMF working paper 2012, Vollgeld 2018, Positive Money UK ongoing, NEED Act USA 2011, Sigurjónsson Report Iceland 2015) includes specific safeguards designed exactly to prevent the Zimbabwe scenario:

- Rule-bound money creation — the money authority cannot expand money at the discretion of politicians. The formula is in the legislation. Often constitutional.

- Constitutional entrenchment — changing the rules requires a referendum or supermajority, not a cabinet meeting.

- Independent monetary authority — insulated from executive capture.

- Optional gold or commodity backing — anchors money to real value.

- 100% reserve banking — abolishes commercial bank credit creation, which Zimbabwe still had.

- Public quarterly audit — forces transparency on the money authority’s operations.

Zimbabwe had none of these. Zimbabwe had: discretionary central bank, political capture, commercial bank credit creation on top, no constitutional constraint, collapsing productive economy, no external backstop. The combination is what produced the catastrophe.

If Zimbabwe had been operating under, say, the Vollgeld system that Switzerland voted on in 2018, the money supply could not have expanded beyond the formula. Politicians could not have ordered the central bank to print. Commercial banks could not have added credit on top. The hyperinflation would have been mathematically impossible — assuming the productive economy collapse was somehow still resolved.

The Quiet Reframe

Zimbabwe is the strongest argument FOR constitutional sovereign money, not against it. The system that destroyed Zimbabwe is the system we still have.

Every safeguard the sovereign money proposals include exists precisely to prevent another Zimbabwe. The scare uses Zimbabwe to defend the system that produced Zimbabwe.

A Quiet Invitation

If this is the first time you’ve heard Zimbabwe explained as something other than “government printed money,” get the next post in your inbox.

Every Other Famous Hyperinflation Followed The Same Pattern

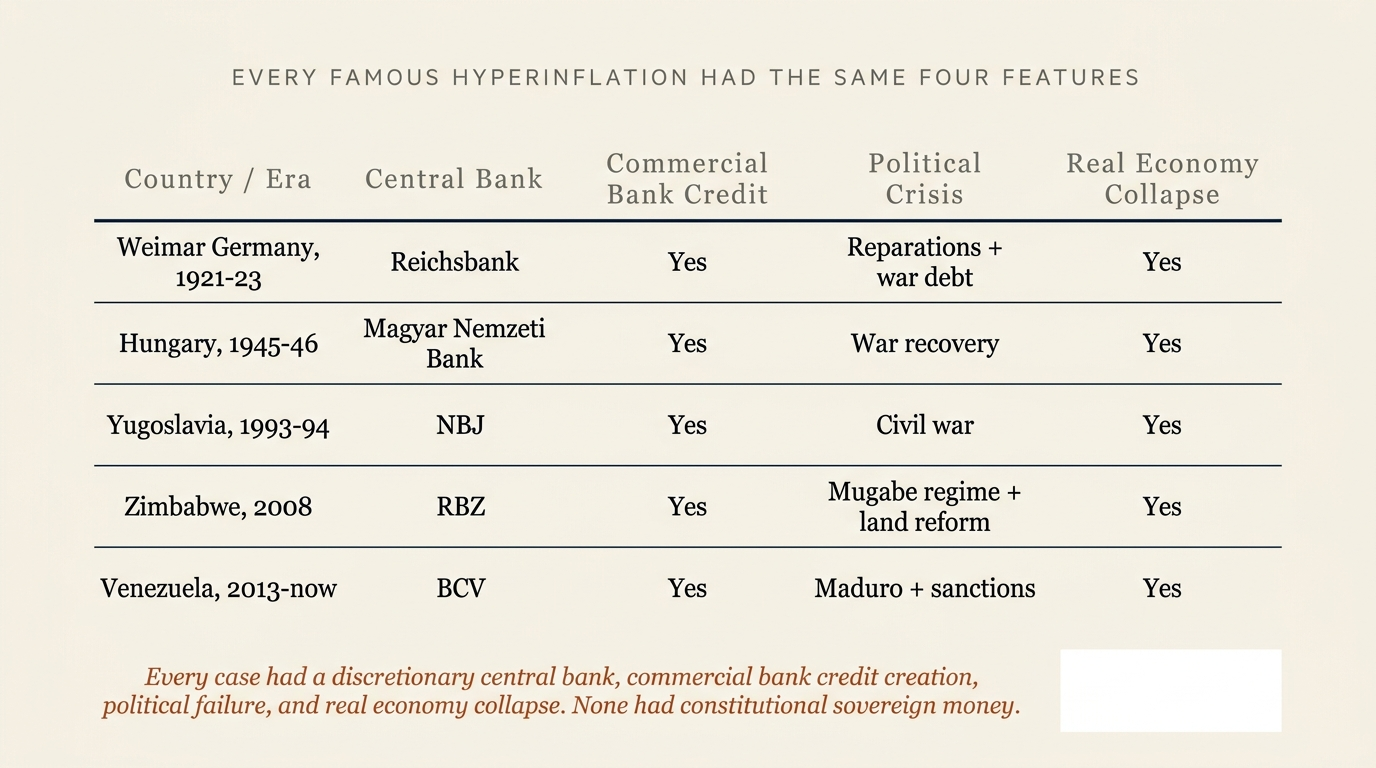

Pick any famous hyperinflation. Same four features.

Weimar Germany (1921-23). Reichsbank with political pressure to print. Commercial bank credit expansion alongside. Reparations payments forcing currency conversion. Real economy battered by war debts. No sovereign money system. Hyperinflation.

Hungary (1945-46). The Magyar Nemzeti Bank with full discretion. Commercial bank credit creation. Post-war reconstruction stress. Productive economy destroyed by war. Holds the record for the worst monthly inflation rate in history. No sovereign money system.

Yugoslavia (1993-94). Central bank under wartime command. Commercial credit. Civil war. Productive economy in collapse. Hyperinflation.

Venezuela (2013-now). Banco Central de Venezuela with political pressure. Commercial bank credit. Oil price collapse + Maduro government + US sanctions. Productive economy strangled. Multi-year hyperinflation continuing.

Every case had the same four features: discretionary central bank, commercial bank credit creation on top, political crisis or capture, real economy collapse. There is not a single case of constitutional, formula-bound, rule-of-law-protected sovereign money producing hyperinflation. There has never been one. The historical record on sovereign money is empty of bad outcomes because it has barely been tried.

The most-cited recent example of formula-bound sovereign issuance in practice was the Pennsylvania colonial currency between 1723 and 1764, which produced one of the most prosperous and stable economies in colonial history. The model failed in some other colonies that abandoned the rule, exactly as the framework predicts.

The Inoculation

Next time someone says “but Zimbabwe,” here is what you can do.

Ask them what Zimbabwe actually had at the moment of the hyperinflation. Not what they have read in a brief news story. Actually had.

The answer is: a central bank, commercial banks creating credit on top, no constitutional constraint, a collapsing productive economy, and no external backstop. Then ask them which of these features sovereign money proposals KEEP and which they REMOVE.

The honest answer is that sovereign money proposals remove the discretionary central bank (replaced with a rule-bound public mint), remove the commercial bank credit creation (replaced with 100% reserve banking), and add the constitutional constraint (replaced “trust the politicians” with “the rules are in the constitution”). Three of the five Zimbabwe failure features are explicitly prevented by sovereign money proposals.

The remaining two — political crisis and productive economy collapse — are downstream of broader policy failure, not of monetary architecture. A society that experiences a civil war or a productive economy collapse will struggle regardless of its monetary system. But “Zimbabwe” as a banking-reform scare is invoking the monetary architecture, not the underlying political collapse. The scare uses Zimbabwe to defend the very monetary system Zimbabwe had.

The scare is, on inspection, an own goal.

The system that destroyed Zimbabwe is the system we still have. The cure for Zimbabwe was constitutional sovereign money. It was not “keep doing what Zimbabwe was doing, but more carefully.”

— The structural sentence of the post.

Three Questions Everyone Should Ask

The Zimbabwe scare makes these three questions impossible to dodge.

Get The Next Post By Email

One plain-English post at a time. No tracking pixels. No advertising. Unsubscribe in one click. Your email goes to [email protected] and nowhere else.

Have you noticed yet?

Frequently Asked Questions

Wasn’t Mugabe’s government printing money DIRECTLY?

The Reserve Bank of Zimbabwe expanded base money. Mugabe’s government pressured the RBZ to do so. But the RBZ retained legal discretion over how much — it was not constitutionally constrained. Commercial banks then expanded credit on top, multiplying the broad money expansion. The “Mugabe printed money” framing is correct in headline but obscures that the multiplier through commercial banks was structural, not Mugabe-controlled.

Wouldn’t a public mint just be a Zimbabwe-style central bank with a different name?

Only if it had discretionary authority. The sovereign money proposals all involve formula-bound issuance, not discretionary. Money creation is tied to GDP growth, productivity, or commodity reserves. The amount is calculated, not chosen. A politician cannot order the mint to print, the way the Mugabe regime ordered the RBZ. Constitutional entrenchment makes the rule hard to change.

What if a future Australian government tries to override the rule?

A constitutional protection makes that legally difficult. Most sovereign money proposals require a national referendum to change the formula. Australia has had referenda before and they are hard to win. The combination of constitutional rule, referendum requirement, and audit transparency is designed to make it harder to abuse than the current arrangement.

Hasn’t Modern Monetary Theory advocated unlimited government spending?

Modern Monetary Theory (MMT) is a different proposal. MMT argues that government spending creates the money it needs and is constrained only by inflation. MMT advocates more discretion, not less. NoticedYet does not advocate MMT. The sovereign money proposals discussed here are rule-bound and bind public money creation by formula. The two approaches are often confused but are technically distinct.

What about countries like Switzerland that nearly voted yes — would they have worked?

The Vollgeld initiative had specific text. The Swiss National Bank would have been the sole money creator. Commercial banks would have lost the right to create deposits through lending. Money creation would have been formula-bound. New money would have been distributed to government and citizens debt-free. The proposal had been studied for years. It would not have produced Zimbabwe; it would have produced a more disciplined version of the current Swiss system.

Where can I read more about the actual Zimbabwe story?

Steve H. Hanke’s research at Johns Hopkins on the chronology of Zimbabwean hyperinflation is the most cited contemporary source. The IMF, World Bank, and Bank of Zambia (which dealt with Zimbabwean currency flight) all have public materials. Sources at the bottom of this post.

About The Author

M. Notice

M. Notice writes NoticedYet, a calm, sourced blog about how private commercial banks create money out of nothing and what that means for the rest of us. The pen name is a voice choice, not opsec. Every post is primary-source-anchored. No products endorsed. No politicians backed.

Reach out: [email protected]

Sources

- McLeay, Radia, Thomas. “Money creation in the modern economy.” Bank of England Quarterly Bulletin, Q1 2014.

- Hanke and Krus. “World Hyperinflations.” Johns Hopkins Institute for Applied Economics, 2013.

- Benes, Kumhof. “The Chicago Plan Revisited.” IMF Working Paper WP/12/202, August 2012.

- Verein Monetäre Modernisierung (MoMo). Vollgeld-Initiative documentation, Switzerland 2018.

- International Monetary Fund. Zimbabwe country reports and historical economic data.

- Joseph Huber. Sovereign Money: Beyond Reserve Banking. Palgrave Macmillan, 2017.

- Positive Money UK. Sovereign money campaign and detailed policy papers.

Historical claims about Zimbabwe and other hyperinflation cases are based on published economic literature. Numerical claims (e.g., the 89.7 sextillion percent peak month-over-month figure) are widely cited but methodologically debated; the order of magnitude is not in dispute. Linked content may move or be updated without notice. This article is general information and analysis only and is not financial, economic, or legal advice. Please verify the primary sources for yourself — that is half the point.