Money From Nothing

Have a look at this paragraph. It’s from a 2014 paper published by the Bank of England’s own quarterly bulletin. Three of their senior staff wrote it. The orthodox financial press did not cover it. Almost nobody in the public has ever read it.

The Bank wrote, about itself, about the banking system it presides over:

It’s worth reading twice. The bank creates new money whenever it lends. New money. Not transferred from a saver. Not borrowed from somewhere else. Created. By the bank. At the moment the loan is written.

This is the orthodox view of how money works in every modern economy. The Federal Reserve operates the same way. So does the European Central Bank, the Bank of Japan, the Bank of Canada, the Swiss National Bank, the Reserve Bank of India, the People’s Bank of China — every central bank presides over a commercial-bank system that does this. The textbooks are slowly being updated. The public, as a rule, has never been told.

What Actually Happens When You Sign A Mortgage

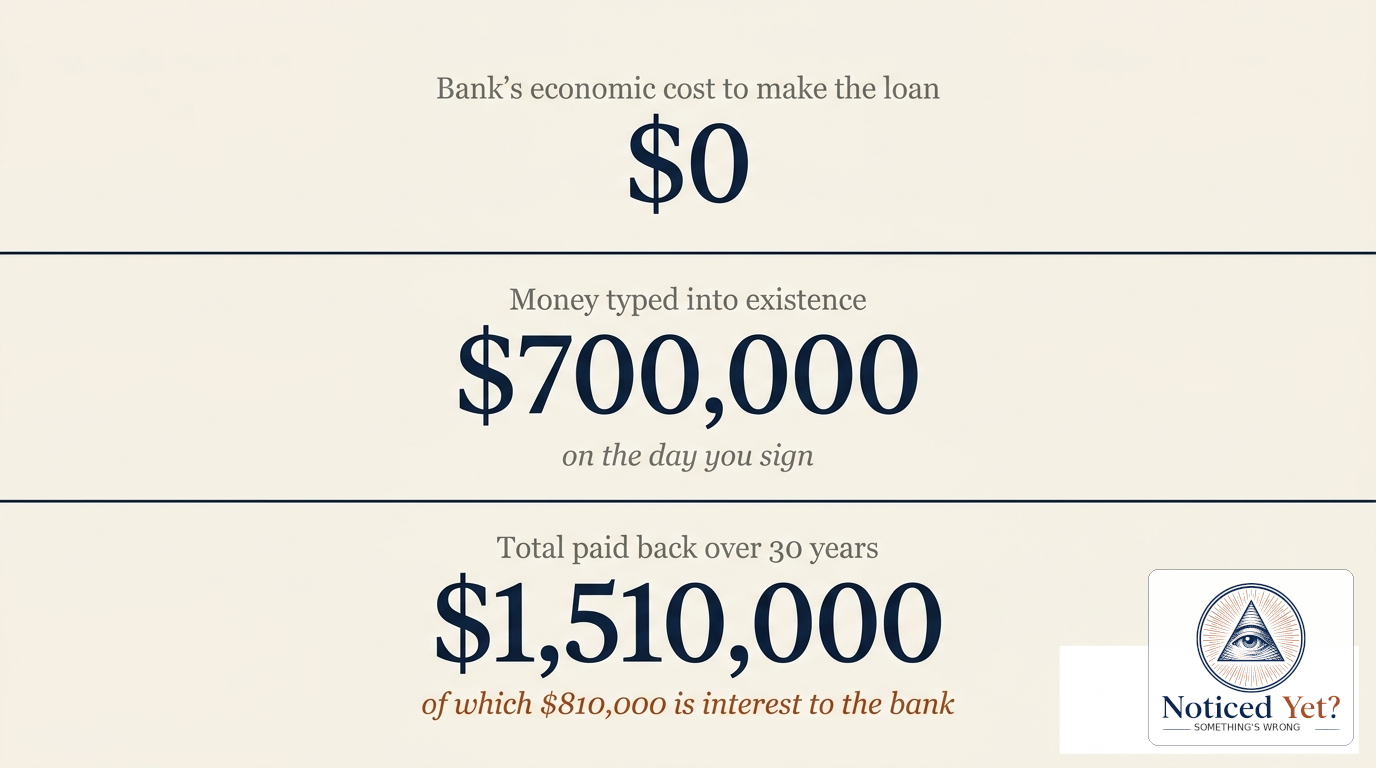

Imagine you walk into a major commercial bank to sign for a $700,000 mortgage on a small flat. You’re nervous. You’re stretching. You’re committing thirty years of your working life.

Behind the counter, the loan officer doesn’t go to a vault. Doesn’t transfer money from somebody else’s account. Doesn’t call the central bank to get the cash.

They type the number into a computer. Your account gains $700,000. The bank’s balance sheet gains a matching liability for the same amount. Both sides expanded by exactly the amount you “borrowed.”

Five seconds before you signed, that $700,000 did not exist anywhere in the economy.

Now it does.

You spend the next thirty years working real hours, doing real labour, in order to repay it. With interest. Real money — earned through real shifts and real overtime — flows back to the bank that conjured the loan into existence with a keystroke.

The Headline Number

97%

of money in circulation in the United Kingdom is created by private commercial banks. Only about 3% is physical cash issued by the Bank of England. Other major economies sit close to the same ratio: the eurozone, the US, Japan and Canada all run between 92–97% bank-money / 3–8% central-bank-money.

Sources: Bank of England Quarterly Bulletin Q1 2014; ECB Monetary Developments statistics; Federal Reserve H.6 release; Bank of Japan monetary base data.

A Quick Number That Should Make You Sit Down

Pick any standard mortgage at a typical recent rate. Use the 30-year term and a 6% interest rate. Here is what the math looks like, from the day you sign to the day you finish repaying:

The bank started with nothing. Over 30 years, they receive $1.5 million of your real labour. Their operational cost — staff, computers, rent, regulatory compliance — comes to maybe 1–2% of the gross take, on a generous estimate. The rest is profit on an act that, when stripped of the legal architecture around it, was the act of typing a number into a screen.

Imagine if you went to your local bakery, the baker scribbled a receipt for $700,000, handed it to you, and then said: “Pay me $4,200 a month for thirty years.”

You would call the police.

Now imagine if the baker had a federal banking licence. The receipt would be called a mortgage. The thirty years of payments would be called responsible homeownership. And the baker’s quarterly profit announcement would be called good economic news.

The only difference between the two is the licence.

What This Used To Be Called

For most of human history, the act we just described was illegal. Not “frowned upon” — illegal.

The Romans called it forgery. The medieval Church called it fraud and theft, compounded. The Quran prohibits riba — the charging of interest, particularly on money that was not the lender’s to begin with. The Torah forbids it among brothers and instructs every fiftieth year to be a Jubilee, in which debts are cancelled outright. Aristotle, in his Politics, called the breeding of money by money “the most unnatural” form of wealth.

Every era of human moral reasoning before the year 1694 condemned the practice of creating money that did not exist and lending it at interest. They condemned it as deeply as any other economic crime they could conceive.

“Of all modes of getting wealth, this is the most unnatural.”

— Aristotle, on lending money at interest. Politics, Book I, ca. 4th century BC.

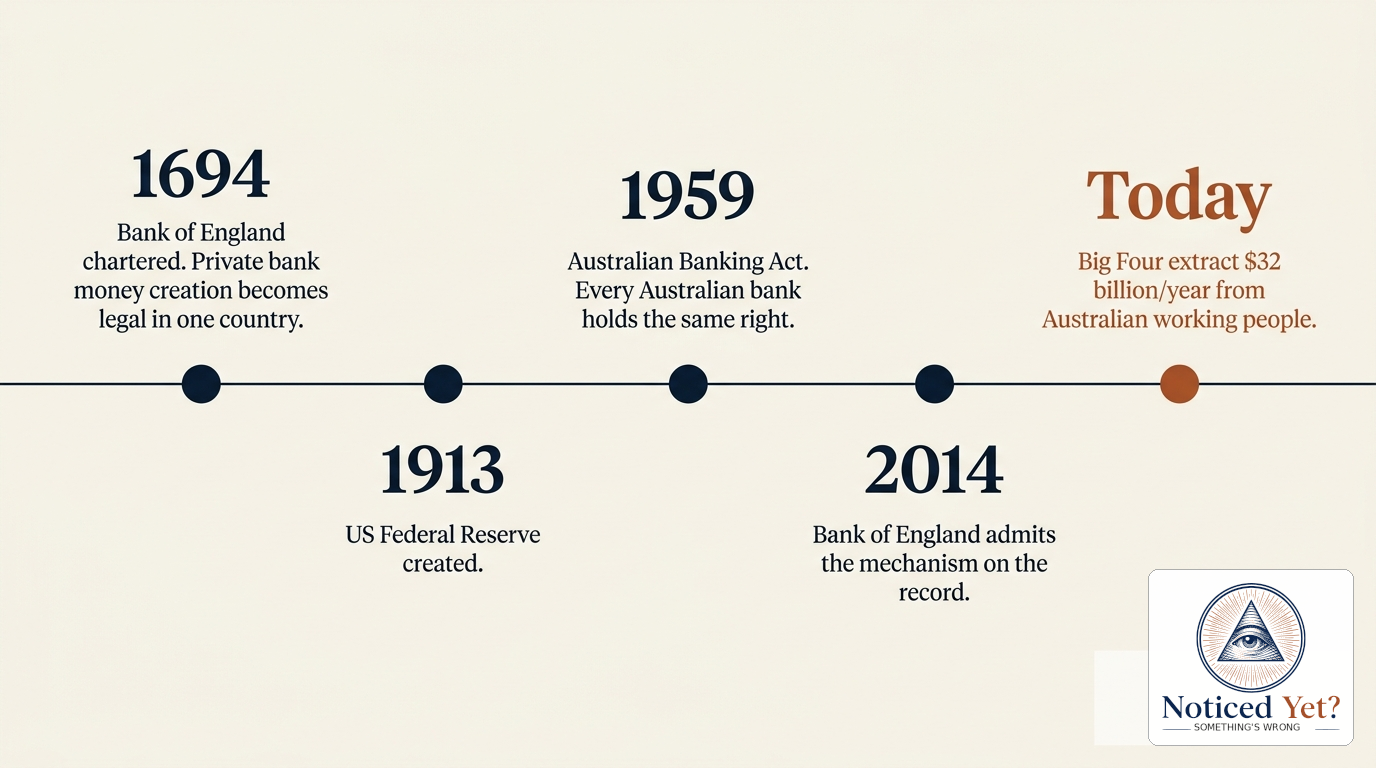

In 1694, the Bank of England received its royal charter. The English crown, broke from foreign wars, accepted a private syndicate’s offer: in exchange for lending the crown £1.2 million in fresh notes, the syndicate received a perpetual licence to issue notes against assets they did not have. Private bank money creation became legal in one country, for the first time. It would not be reversed.

By 1913, the United States set up the Federal Reserve on essentially the same model. Over the next century, every major economy — Britain, France, Germany, Japan, Italy, Spain, the Netherlands, Canada, Australia, New Zealand, Switzerland, Sweden, Norway, the Asian “tigers,” and most of South America — either inherited or wrote their own version of the same Bank Act. By the late twentieth century, every member country of the IMF was running a variation of the 1694 model.

The act did not change. It is the same act it was in Babylon. It is the same act it would be if you tried it tonight in your garage, with a printer. What changed was who’s allowed to do it. And that change is everything.

How The 1694 Model Went Global

In every country listed above, the legal right is the same. The mechanism is the same. The beneficiary class is the same.

A Quiet Invitation

If you’ve never seen any of this before, you’re going to want the next one in your inbox.

The Cost To You — In Dollars You Recognise

The act of money creation doesn’t just affect borrowers. It affects every person who holds money.

When the bank types $700,000 into your account, that $700,000 enters the economy. It chases the same houses, the same groceries, the same petrol that everyone else’s money is chasing. Add up all the loans made across a national economy in a given year — in the US that’s around $3 trillion of new bank credit on average, in the UK around £200 billion, in the eurozone close to €500 billion — and the total money supply expands faster than the supply of real goods and services. Prices rise.

That’s what inflation is. Not an act of nature. Not an external shock. A consequence of new money being created by banks at a faster rate than the economy is producing things to spend it on.

You earn the median wage in your country — say $50,000 a year, after tax around $40,000. You save 10% of that — $4,000 a year. You put it in a savings account paying 3%.

That looks responsible. It looks like the right thing to do.

But last year your grocery shop went up 6%. Your insurance went up 9%. Your rent went up 8%. Your $4,000 buys less than it did a year ago. You earned 3%. You went backwards.

Meanwhile, the borrower with the big mortgage actually wins from this. Their house is worth more in nominal terms. Their debt buys less in real terms. They are paying back the bank in dollars that have lost purchasing power.

The saver loses. The leveraged property owner gains. The bank, who issued the credit that did both, takes a clip on the way through. This isn’t a flaw in the system. It is the operating principle of the system.

A Quiet Question Worth Asking

Why does a private business get this right?

Money is a public utility. Its supply determines the value of every wage, every pension, every retirement balance, every house, every cup of coffee. Expanding or contracting the money supply is one of the deepest powers a society can grant.

In every developed economy, we have granted that power to a small handful of publicly-listed commercial banks. In the United States it’s the half-dozen money-centre banks — JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, Goldman Sachs, Morgan Stanley. In Britain it’s the “big four” of Lloyds, Barclays, HSBC, NatWest. In Germany the dominant lenders are Deutsche Bank and Commerzbank. In Japan it’s the three megabanks — MUFG, Mizuho, SMFG. The pattern is the same: a few private companies, each making tens of billions in profit per year, the majority of which is generated by the act of money creation itself.

Almost universally, a significant share of that profit flows offshore — to Vanguard, BlackRock, State Street, sovereign wealth funds, and a long tail of international institutional investors who hold the float across borders.

The Number Nobody Adds Up

$500B+

Combined annual profit, in the most recent reporting cycles, of the world’s twenty largest commercial banks — JPMorgan Chase, ICBC, Bank of America, Agricultural Bank of China, China Construction Bank, Citigroup, Wells Fargo, HSBC, BNP Paribas, Mitsubishi UFJ, and a dozen others. The majority of that profit is generated by the act of money creation: typing loans into existence and collecting interest on them.

Sources: bank annual reports; BIS Statistics on global banking; IMF Financial Soundness Indicators.

No referendum was ever held on this arrangement, in any country. No constitutional clause was ever drafted to authorise it. The right was granted gradually, by acts of national parliament, often in committee meetings that were never reported on. In the United States, the Federal Reserve Act of 1913 passed two days before Christmas, on a near-empty Senate floor. In Britain, the original 1694 charter was a four-page document slipped through the Commons. In Australia, the 1959 Banking Act amendments went through with bipartisan support and no media coverage. The pattern repeats.

It is the most consequential delegation of public power in the history of every nation that did it. And most citizens of those nations have never heard of it.

“But Hasn’t This Been Studied? Surely Economists Have Looked At This?”

They have. And the alternatives have been modelled and tested.

In 1933, three University of Chicago economists — Irving Fisher, Henry Simons and Frank Knight — published A Program for Monetary Reform. The proposal: end private money creation; make the central monetary authority the only issuer of money; banks become true intermediaries, lending what real savers have deposited. The plan was signed by 235 American economists and submitted to President Franklin D. Roosevelt. He read it. He didn’t act on it. The banking lobby made sure it stayed buried.

In 2012, two IMF economists — Jaromir Benes and Michael Kumhof — published The Chicago Plan Revisited. They ran the proposal through modern computational economic models. Their conclusion was that under a sovereign money system: government debt could be paid down to near zero; financial crises virtually eliminated; output could rise by approximately 10%. The paper was published as IMF Working Paper WP/12/202. It is freely available on the IMF’s website. The financial press did not cover it.

In 2018, Switzerland held a national referendum on a constitutional amendment that would have abolished private bank money creation. Twenty-four percent of Swiss voters voted yes. They lost, but they did so under conditions of overwhelming opposition: the Swiss National Bank, every major Swiss bank, every major political party, and an estimated 26-to-1 spending advantage by the “no” campaign were all arrayed against them.

The Vollgeld initiative, as it was known in German, had been built on years of patient public education. It nearly won.

Similar reform proposals have been documented in the United States (the NEED Act, 2011), Iceland (the Sigurjónsson Report, 2015), the United Kingdom (Positive Money’s submissions to multiple parliamentary inquiries), and the European Parliament (sovereign-money hearings, 2017–2019). None have yet succeeded. None have been technically refuted.

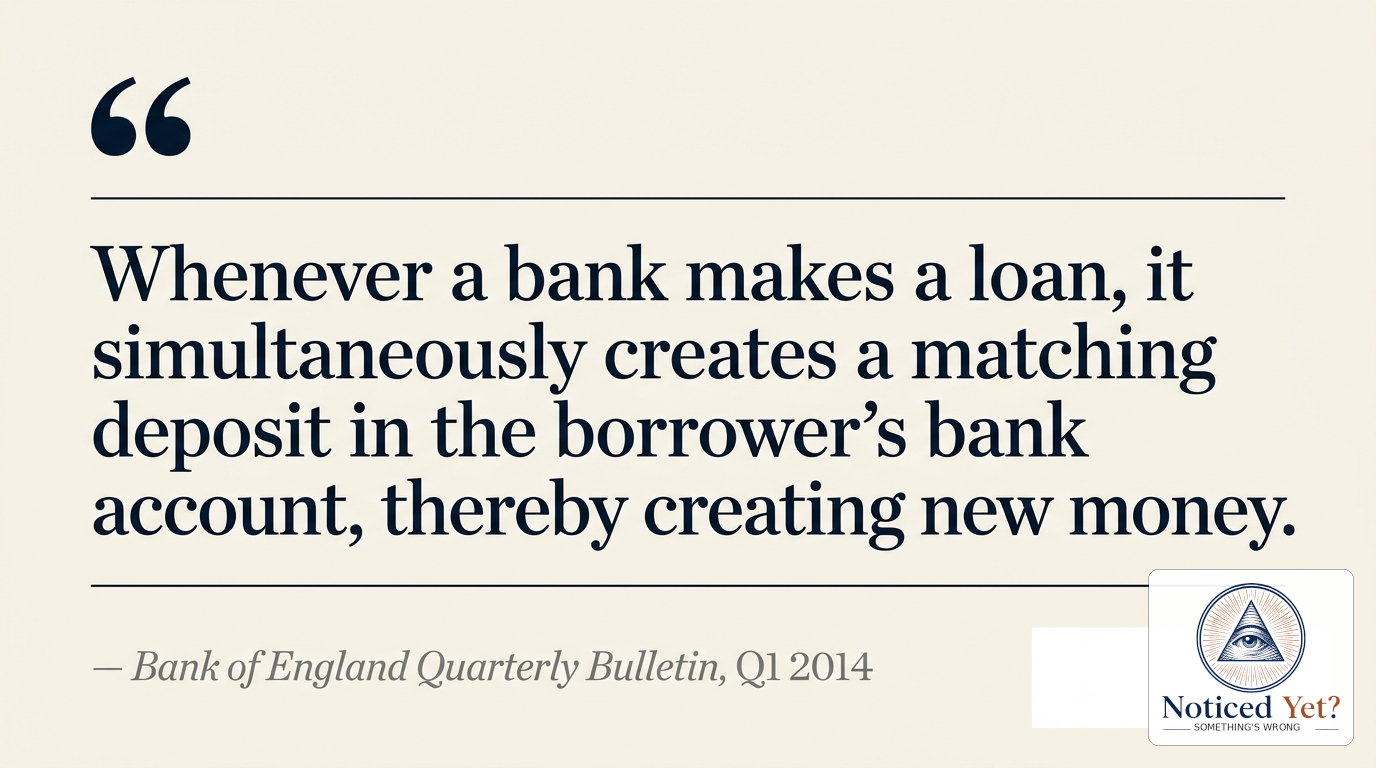

“Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money.”

— McLeay, Radia, Thomas. Bank of England Quarterly Bulletin, Q1 2014.

These reform efforts — the Chicago Plan, the IMF working paper, the Vollgeld vote, the NEED Act, the Sigurjónsson Report — are the documented intellectual tradition of an alternative to the system we live under. None of them have ever been refuted on technical grounds. They have only ever been delayed, redirected, or quietly buried.

Three Questions Everyone Should Ask

The hard work of this blog is making a distinction the banking lobby would prefer you never made. Three questions, not one. Kept separate on purpose.

You Have Two Reactions Available

Either:

- Money creation by private banks is fine. The system is working. Half a trillion dollars of annual global bank profit from money creation is just the cost of doing business.

- Something is structurally wrong here. The right is the wrong right to delegate to private firms. The people who run this system owe the rest of us an answer.

Pick one. There is no third option that survives one hour of honest reading.

The Bank of England admitted the mechanism. The IMF modelled the fix. The Swiss nearly voted it in.

The licence makes it legal.

The rest is up to you.

Why This Blog Exists

Banking-critical journalism in every English-speaking country is structurally underfunded. Major commercial banks are among the largest advertisers in mainstream media in every country; editorial coverage reflects that. The Bank of England 2014 paper, the IMF 2012 paper, and the 2018 Vollgeld vote each received almost no significant press attention in the US, UK, Canada, Australia, New Zealand, Ireland, South Africa, India, or anywhere else they should have made the front page.

NoticedYet exists to fix one small part of that gap. Calm, sourced, plain-English coverage of how money is actually created and who benefits — written so a reader anywhere in the world can recognise the same mechanism running in their own country. No products endorsed. No politicians backed. No tribes attacked. The villain is always the banking licence, never any group.

If the case lands, share it. If it doesn’t, write back.

What We Do Here

Three pillars. Roughly half the posts are The Critique — what banks actually do, with primary sources. Roughly half are The Inoculation — patient demolitions of the scare arguments the banking lobby uses against reform. The rest are The Constructive — what a sovereign money system would actually look like, drawn from the Chicago Plan, the IMF working paper, the Vollgeld proposal, and Joseph Huber’s Sovereign Money.

Every post is sourced. Every claim has a receipt. Every closing line is meant to stick. The writing is calm on purpose — the facts do the work, not the volume.

This is not financial advice. We do not tell you what to buy, hold or sell. We just show you the structure that is rarely shown in plain English.

Get The Next Post By Email

One plain-English post at a time. No tracking pixels. No advertising. Unsubscribe in one click. Your email goes to [email protected] and nowhere else.

Have you noticed yet?

Read Next

If this is the first time you have seen the mechanism explained plainly, two further posts go where this one leaves off:

- Why The Lost Man In The Desert Pays Twice For The Same Water — the cleanest single-page explanation of inflation. Three minutes.

- Where The First $380,000 Of Your Mortgage Payments Actually Go — the maths of where your money actually goes in the first decade.

Frequently Asked Questions

Is this really how banking works? It sounds almost unbelievable.

Yes. It is the orthodox view of every central bank and serious monetary economist in the world. The Bank of England’s 2014 paper Money creation in the modern economy is the cleanest single-source statement of the mechanism. Read it yourself, link in Sources below.

If banks can create money, why don’t they create as much as they want?

They are constrained by three things — capital requirements (set by national prudential regulators under the Basel III framework), regulatory liquidity ratios, and demand from borrowers. None of these constraints stop money creation; they only meter it.

Is what banks do actually illegal in some technical sense?

No. The Banking Acts in every developed economy give chartered commercial banks the legal right to take deposits and make loans. The right to create the money those loans consist of is implicit in the legal framework. Without a licence, doing the same thing would be counterfeiting and fraud. With a licence, it’s banking.

Why hasn’t this been front-page news?

Mainstream media in every English-speaking country depends heavily on bank advertising revenue. Major commercial banks are among the largest advertisers in every major publication. Editorial coverage of banking is correspondingly soft. The Bank of England 2014 paper, the IMF 2012 paper, and the 2018 Vollgeld vote each received negligible press coverage in the US, UK, Canada, Australia, New Zealand, Ireland, and beyond, despite their importance.

Doesn’t the central bank control the money supply?

No central bank does. The Federal Reserve, ECB, Bank of England, Bank of Japan and others set the policy rate — the price of money. They don’t directly control the quantity. Commercial banks create most of the broad money supply through their lending decisions. The central-bank toolkit is indirect.

What can be done about it?

That is the subject of every constructive post on this blog. Short version: the answer that serious economists have studied since 1933 is sovereign money — making money creation a public function bound by formula, returning the seigniorage to citizens. It is, deliberately, not a quick answer. There is no quick answer.

Where can I read more?

Sources at the bottom of this page. Start with the Bank of England 2014 paper if you read nothing else.

About The Author

M. Notice

M. Notice writes NoticedYet, a calm, sourced blog about how private commercial banks create money out of nothing and what that means for the rest of us. The pen name is a voice choice, not opsec. Every post is primary-source-anchored. No products endorsed. No politicians backed.

Reach out: [email protected]

Sources

- McLeay, Radia, Thomas. “Money creation in the modern economy.” Bank of England Quarterly Bulletin, Q1 2014.

- Benes, Kumhof. “The Chicago Plan Revisited.” IMF Working Paper WP/12/202, August 2012.

- Bank for International Settlements. Statistics on global banking, credit aggregates, and money supply across reporting jurisdictions.

- Federal Reserve. H.6 Money Stock Measures — weekly release on US money aggregates.

- European Central Bank. Monetary aggregates and counterparts statistics — eurozone money supply data.

- IMF Working Papers archive. Multiple monetary-economics working papers on bank money creation, capital regulation, and financial stability.

- Vollgeld-Initiative.ch. Original campaign documents from the 2018 Swiss sovereign-money referendum (English translation).

- Positive Money. UK-based research and advocacy organisation on monetary reform — reports, parliamentary submissions, and analysis.

- Wikipedia. “Chicago Plan” — overview and bibliography for Fisher, Simons, Knight, 1933.

Disclaimer

The numbers in this article are illustrative, calculated against typical recent mortgage parameters in developed-economy markets. Actual rates, terms, and amortisation schedules vary by lender, country, and product. Linked content may move or be updated without notice. This article is general information and analysis only and is not financial, mortgage, tax or investment advice. Always seek advice suited to your personal circumstances from a qualified, fee-only adviser whose interests are not tied to product sales. Please verify the primary sources for yourself — that is half the point.